•

•

GBP and EUR Account for Marshall Islands Company: Access UK and EU Payment Rails

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

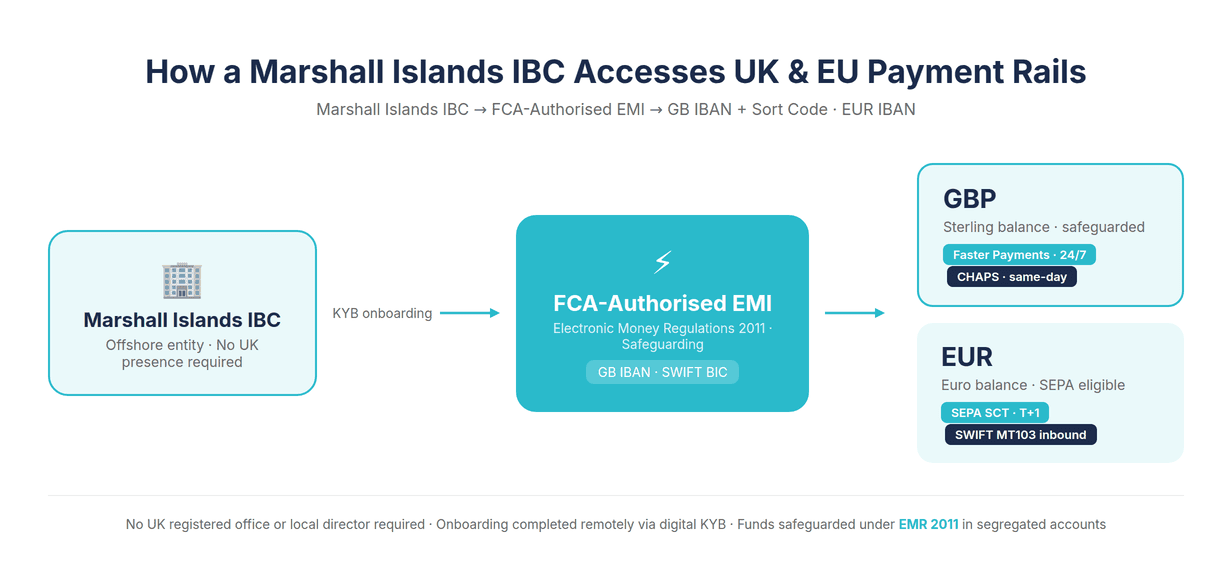

A Marshall Islands company can obtain a UK sort code and EUR IBAN through an FCA-authorised electronic money institution (EMI) — without a UK registered office, local director, or physical presence. For directors of Marshall Islands International Business Corporations (IBCs) trading with UK clients or settling invoices with EU suppliers, a Marshall Islands company GBP EUR account UK represents a practical, regulated solution that most traditional banks will not offer.

The structural barrier is well documented. UK and EU banks routinely decline Marshall Islands entities — not because the jurisdiction is non-compliant, but because offshore Pacific IBCs fall outside the onboarding models most banks have built. The result: GBP receipts arrive via costly correspondent banking, and SEPA payments require a workaround that adds time and fees to every transaction.

This article explains how a Marshall Islands IBC gets a UK sort code, how EUR IBAN access through a UK-based EMI works in practice, what KYB documentation is required, and how GBP and EUR payment flows operate together.

[aa key-takeaways]

Key Takeaways

A Marshall Islands IBC can hold a GB IBAN and UK sort code through an FCA-authorised EMI under the Electronic Money Regulations 2011 — no UK office required.

GB IBANs issued by FCA-authorised EMIs are eligible for SEPA Credit Transfer (SEPA SCT) provided the EMI is a SEPA scheme participant.

Payment rails available include Faster Payments (up to £1,000,000 per transaction, real-time), CHAPS (same-day, high-value), and inbound SWIFT MT103.

SEPA SCT settles same-day or T+1; SEPA Instant (SCT Inst) settles in under 10 seconds with a €100,000 per transaction cap.

Onboarding is completed digitally — certificate of incorporation, UBO declaration, and source of funds documentation are the core requirements.

[aa btn]Book a Call[/aa]

[/aa]

Why Marshall Islands Companies Cannot Access UK and EU Banking Directly

UK banks classify Marshall Islands entities in the same high-risk tier as other Pacific offshore jurisdictions — meaning near-100% rejection rates for account applications, regardless of the legitimacy of the business. This is not a regulatory prohibition. There is no UK law preventing a Marshall Islands IBC from holding a bank account. The barrier is structural: banks have built onboarding systems around domestic or EU-registered entities, and offshore Pacific IBCs fall outside those systems by design.

How UK Banks Classify Marshall Islands Entities

When a Marshall Islands IBC applies to a UK bank, the compliance team must perform enhanced due diligence on an offshore structure with no physical presence in the UK, no domestic tax filings, and no local regulatory footprint. Most UK banks have not built the operational capacity to manage this level of enhanced due diligence at scale. The result, as documented in BIS research on correspondent banking, is that banks exit or decline offshore relationships systematically rather than assess them individually.

The Marshall Islands was removed from the EU offshore blacklist in October 2019, having implemented EU information exchange requirements. The jurisdiction is FATF-compliant. The banking access problem is not a compliance failure — it is a cost-benefit decision by banks that GBP accounts for offshore companies are not worth the compliance overhead.

The Correspondent Banking Alternative and Its Limitations

Marshall Islands IBCs that cannot access a direct UK bank account often receive GBP through correspondent banking channels. This means inbound SWIFT MT103 transfers, typically settling in 1–3 business days, with fees deducted at each correspondent bank in the chain. For an IBC invoicing a UK buyer, the practical outcome is that GBP arrives late, short of the invoiced amount, and without the real-time settlement that UK counterparties expect from domestic payments.

A GBP account for an offshore company issued by an FCA-authorised EMI removes this overhead entirely. The IBC holds a named UK sort code and account number. UK clients pay via Faster Payments — the same rail used for domestic transfers — and funds settle within seconds. EQWIRE has covered this mechanism in detail for comparable structures, including its guide to a UK payment account for offshore companies such as Bermuda-incorporated entities.

What GBP Sort Code and EUR IBAN Access Actually Unlocks

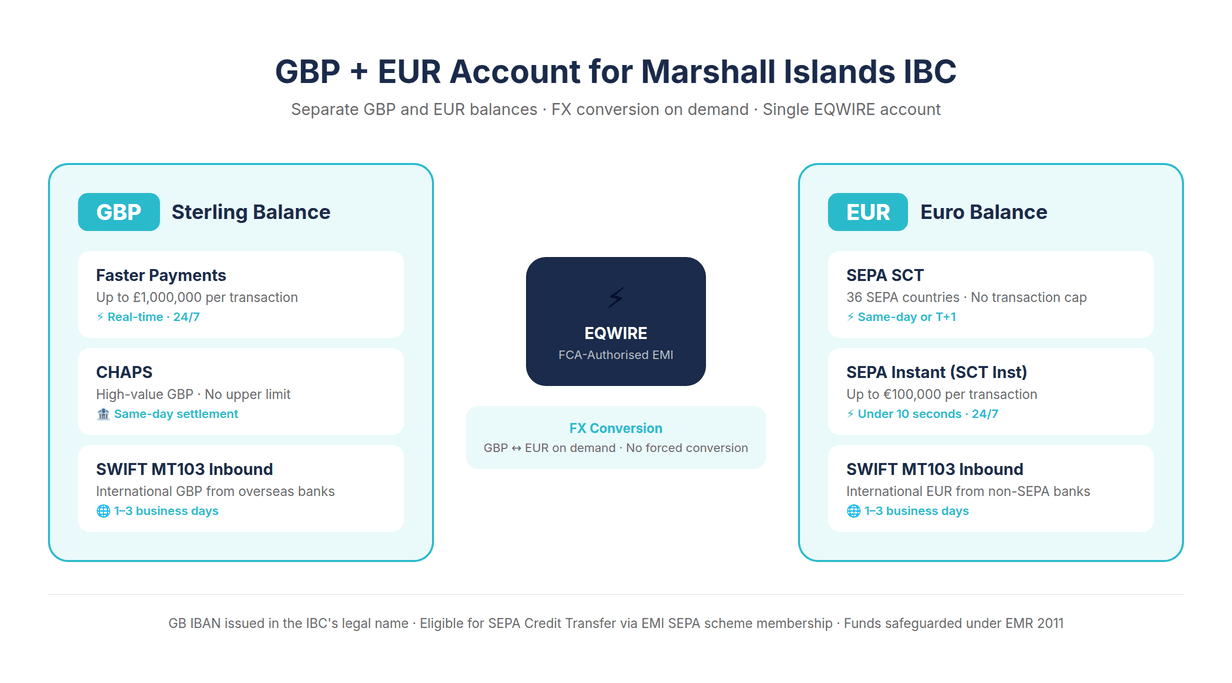

A Marshall Islands IBC GBP EUR IBAN sort code combination changes the payment infrastructure available to the business. Inbound GBP from UK clients settles in real time. Outbound EUR to EU suppliers routes via SEPA SCT, typically same-day or T+1. FX conversion between GBP and EUR can be executed on demand without forced conversion at receipt.

How a Marshall Islands IBC Gets a UK Sort Code

An FCA-authorised EMI operating under the Electronic Money Regulations 2011 can issue a UK sort code and account number — a GB IBAN — directly in the name of a Marshall Islands IBC. There is no requirement in the EMR 2011 for the account holder to be a UK-incorporated entity or to maintain any physical UK presence. This is the regulatory basis on which an offshore entity holds a UK sort code and account number — not a workaround, but a separate and fully legitimate class of payment service provider.

What an FCA-Authorised EMI Is and Why It Can Onboard Offshore Entities

An electronic money institution (EMI) is licensed by the Financial Conduct Authority (FCA) under the Electronic Money Regulations 2011 to issue electronic money and provide payment services. EMIs are not deposit-taking banks — they do not offer credit facilities, overdrafts, or FSCS deposit protection. What they provide is fully functional payment account infrastructure: named sort codes, account numbers, IBANs, and access to UK and European payment rails.

The regulatory framework for EMIs does not require their account holders to be UK-incorporated. This distinguishes EMIs from banks, which apply internal onboarding models that typically restrict accounts to entities with a UK or EU presence. FCA-authorised EMIs are required to apply robust KYB and AML procedures, but these apply to account holders regardless of jurisdiction — including Marshall Islands IBCs. For those seeking a UK bank details for offshore companies equivalent, an FCA-authorised EMI delivers precisely this, as detailed in EQWIRE's guide to sort code without a UK office for BVI and similar offshore structures.

Client funds held at an EMI are safeguarded under EMR 2011. EMIs must hold client funds in segregated accounts at an authorised credit institution, separate from the EMI's own funds. This is not FSCS protection, but it is a meaningful regulatory obligation.

GB IBAN Structure and Faster Payments / CHAPS Access

A GB IBAN has the structure GB + 2 check digits + 4-character bank code + 6-digit sort code + 8-digit account number. The sort code identifies the EMI as the account-holding institution. When a UK client initiates a Faster Payments transfer to this sort code and account number, the payment routes through the UK Faster Payments infrastructure, overseen by the Bank of England, and settles in the EMI account in real time — 24 hours a day, 7 days a week.

Faster Payments supports individual transactions up to £1,000,000. For high-value transfers above this threshold, or where same-day certainty is required for high-value settlements, CHAPS (Clearing House Automated Payment System) is available — same-day, with no upper transaction limit for eligible accounts.

[aa fast-fact]

Fast Fact: The Marshall Islands has registered over 100,000 International Business Corporations (IBCs), many of which require GBP access to serve UK-domiciled clients — making FCA EMI accounts the primary practical solution for this market.

[/aa]

SWIFT MT103 for Inbound International Transfers

For inbound GBP arriving from outside the UK — a Hong Kong bank, a US correspondent, or a Singapore-based client — the EMI account supports inbound SWIFT MT103 transfers. Settlement is typically 1–3 business days depending on the correspondent chain, with a SWIFT BIC provided alongside the sort code and account number. This covers the full spectrum of GBP inbound scenarios a Marshall Islands IBC is likely to face.

[aa cta]

Open a GBP Account for Your Marshall Islands Company

EQWIRE issues GB IBANs and UK sort codes to offshore entities, including Marshall Islands IBCs. Onboarding is completed remotely via digital KYB.

[aa btn]Create Account[/aa]

[/aa]

How to Open a EUR IBAN for a Marshall Islands Company

A Marshall Islands IBC can receive a EUR IBAN from a UK-based FCA-authorised EMI that is a member of the SEPA scheme. SEPA (Single Euro Payments Area), as defined by the European Central Bank, covers 36 countries and enables standardised euro transfers. The UK is not an EU member, but UK-based payment institutions that are SEPA scheme participants can issue EUR IBANs eligible for SEPA Credit Transfer — including to offshore entities such as Marshall Islands IBCs.

SEPA SCT Eligibility from a GB-Prefixed IBAN

SEPA access for a Marshall Islands IBC through a UK EMI works as follows: the EMI, as a SEPA scheme participant governed by the European Payments Council (EPC), routes outbound EUR transfers via SEPA Credit Transfer (SEPA SCT). The settlement timeline is same-day or T+1 within the SEPA zone. The Marshall Islands IBC's EUR IBAN carries a GB prefix — this is the IBAN of the UK EMI, reflecting the account's issuing institution, not the IBC's jurisdiction of incorporation.

SEPA SCT is governed by the EPC's SCT Rulebook and covers 36 SEPA member countries. The standard transfer has no transaction cap. Settlement typically completes within one business day, with same-day settlement increasingly common for transfers initiated before the EMI's daily cutoff. The same SEPA access logic applies to other offshore entities — EQWIRE's guide to SEPA access for offshore entities covers the Seychelles IBC case in comparable detail.

SEPA Instant Availability and the €100,000 Transaction Cap

SEPA Instant Credit Transfer (SCT Inst) provides settlement in under 10 seconds, available 24/7. The transaction cap for SEPA Instant is €100,000 per payment. Availability depends on both the sending and receiving institution supporting the SCT Inst scheme — not all EU banks have fully implemented SEPA Instant. For Marshall Islands IBCs settling large EUR invoices above €100,000, standard SEPA SCT is the reliable route.

How EU Counterparties Receive a GB IBAN: What to Tell Them

A GB-prefixed IBAN is eligible for SEPA Credit Transfer provided the issuing EMI is a SEPA scheme participant — unlike a bank account in Germany or France, the GB prefix signals a UK-regulated entity, not an EU-domiciled one. Post-Brexit, some EU counterparties may query a GB IBAN when initiating a SEPA transfer. The practical resolution is straightforward: the Marshall Islands IBC provides the EMI's SWIFT BIC alongside the IBAN, confirms the issuer's SEPA scheme membership, and the transfer processes normally. This is a named IBAN account in the IBC's own legal name — not a pooled or shared structure — which resolves most counterparty queries at first contact.

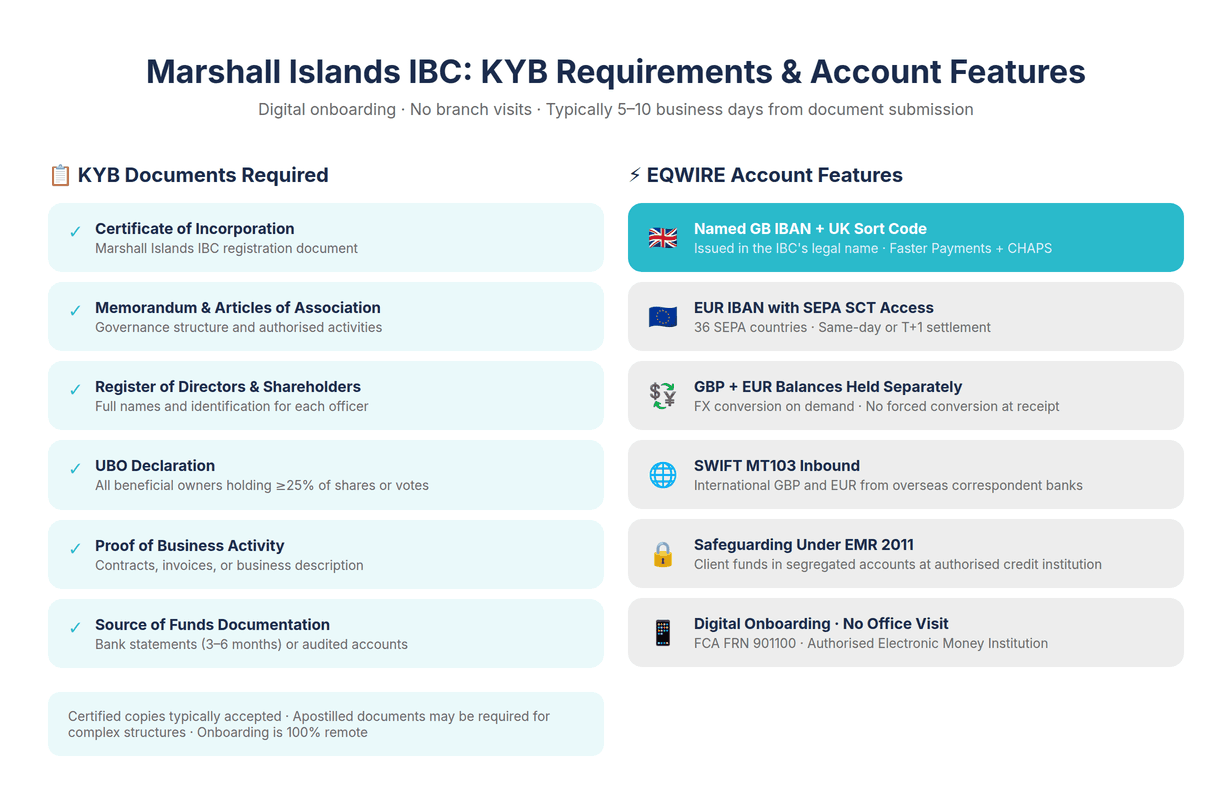

KYB Requirements for Marshall Islands IBC Onboarding

Marshall Islands IBCs applying for a payment account at an FCA-authorised EMI must complete a digital Know Your Business (KYB) process. This involves providing corporate documentation and beneficial ownership information sufficient for the EMI to meet its obligations under the UK Money Laundering Regulations 2017 and the Financial Crime: Financial Sanctions guidance published by the FCA.

Corporate Documents Required

Standard documentation for a Marshall Islands IBC onboarding includes:

Certificate of incorporation — confirming the IBC's legal existence and registration in the Marshall Islands

Memorandum and articles of association — confirming governance structure and authorised activities

Register of directors — full names and identification for each director

Register of shareholders — ownership structure and share classes

UBO declaration — for all Ultimate Beneficial Owners (UBOs) holding 25% or more of shares or voting rights

Proof of business activity — contracts, invoices, or a business description demonstrating the nature of trading operations

Source of funds documentation — evidence of how the IBC generates its revenue

Certified copies are typically accepted. Apostilled documents may be required for some structures, depending on the EMI's KYB policy. Additional documentation may be requested for complex structures such as layered holding companies or nominee director arrangements.

UBO Declaration and Source of Funds

The UBO declaration is a formal statement identifying all natural persons who ultimately own or control the IBC above the 25% threshold. For a Marshall Islands IBC with a single director-shareholder, this is straightforward. For structures involving nominee shareholders, foundations, or multi-layer ownership, the EMI will require documentation tracing beneficial ownership to the natural person level.

Source of funds documentation — bank statements, audited accounts, or a written explanation of revenue sources — is a standard requirement for all offshore entity onboarding. Marshall Islands IBCs with active trading history can typically satisfy this with 3–6 months of bank statements or equivalent evidence.

Ongoing Compliance and Transaction Monitoring

Once onboarded, Marshall Islands IBCs are subject to the same ongoing transaction monitoring as any EMI account holder. The EMI monitors for unusual patterns and may request periodic re-verification. Transaction volume and complexity do not disqualify a Marshall Islands IBC — but IBCs with high-value or high-volume payment activity should expect more detailed source of funds review at onboarding.

Using GBP and EUR Accounts Together: Payment Flows

Once a GBP account and EUR IBAN are live, a Marshall Islands IBC can receive GBP from UK clients via Faster Payments and send EUR to EU suppliers via SEPA SCT — from a single multi-currency Marshall Islands company GBP EUR account UK setup, with GBP and EUR balances held separately.

Receiving GBP from UK Clients via Faster Payments

A Marshall Islands trading company invoicing a UK buyer provides its sort code and account number on the invoice. The UK buyer's bank initiates a Faster Payments transfer, which settles in the EMI account in real time. The IBC's GBP balance updates immediately. There is no correspondent bank fee deducted, no 1–3 day settlement delay, and no uncertainty about the amount received.

This is the operational equivalent of a domestic UK payment — the buyer sees a familiar sort code and account number, and the payment processes identically to any UK-to-UK transfer. For Marshall Islands IBCs with regular UK client receivables, this eliminates the primary friction in their payment cycle.

Sending EUR to EU Suppliers via SEPA SCT

A Marshall Islands consultancy IBC paying a Berlin-based contractor accesses outbound EUR via SEPA SCT from its EUR balance. The contractor's German bank account receives the transfer same-day or T+1, with the exact invoice amount — no correspondent deductions. The IBC provides the contractor's IBAN and BIC; the payment routes directly through the SEPA network.

For high-volume EUR payables — supplier runs, contractor payrolls, platform settlements — SEPA SCT provides the same reliability and cost structure available to EU-domiciled businesses. The Marshall Islands IBC's offshore registration does not affect how the payment appears to the recipient.

Converting Between GBP and EUR Without Forced Conversion

GBP and EUR balances are held separately in the EQWIRE account. A Marshall Islands IBC receiving GBP from UK clients and paying EUR to EU suppliers converts between currencies on demand, at the point of payment, rather than being forced to convert at receipt. This gives the IBC control over FX timing — a meaningful operational and treasury advantage for businesses with regular cross-currency flows.

[aa cta]

Open a Multi-Currency Account for Your Marshall Islands IBC

Hold GBP and EUR in separate balances. Access Faster Payments, CHAPS, and SEPA SCT from a single EQWIRE account.

[aa btn]Create Account[/aa]

[/aa]

EQWIRE for Marshall Islands Companies

EQWIRE is an FCA-authorised EMI that provides GBP and EUR payment accounts to Marshall Islands IBCs and other offshore entities. As a UK-regulated institution operating under the Electronic Money Regulations 2011 (FCA FRN 901100), EQWIRE issues GB IBANs and UK sort codes directly in the company's legal name, with no requirement for a UK office, UK director, or local shareholder.

EQWIRE provides the following to eligible Marshall Islands IBCs:

Named GB IBAN and UK sort code — in the IBC's legal name

GBP Faster Payments (inbound and outbound, real-time, 24/7)

CHAPS (same-day, high-value GBP transfers)

SWIFT MT103 inbound (for international GBP receipts)

EUR IBAN with SEPA SCT access (outbound and inbound)

GBP and EUR balances held separately, FX conversion on demand

Client funds safeguarded in segregated accounts under EMR 2011

Onboarding is completed digitally. A Marshall Islands IBC applying through EQWIRE submits corporate documentation and UBO information via the online KYB process. A FCA EMI account for offshore companies of this type does not require branch visits, notarial appointments, or in-person verification. EQWIRE's offshore accounts series covers similar structures for other jurisdictions, including guides for Bermuda and BVI companies needing UK payment access.

FAQ

What payment rails does a Marshall Islands company get with a UK GBP account?

A Marshall Islands IBC holding a GBP account through an FCA-authorised EMI gets access to three UK payment rails: Faster Payments (real-time, up to £1,000,000 per transaction, available 24/7), CHAPS (Clearing House Automated Payment System — same-day, high-value GBP transfers with no upper transaction limit for eligible accounts), and inbound SWIFT MT103 (for international GBP arrivals from overseas banks, typically settling in 1–3 business days depending on the correspondent chain). The EMI's sort code and account number function identically to a domestic UK bank account from the perspective of the sender.

Can a Marshall Islands IBC send SEPA payments from a GB IBAN?

Yes. FCA-authorised EMIs that are SEPA scheme participants can issue GB-prefixed IBANs that are eligible for SEPA Credit Transfer (SEPA SCT), governed by the European Payments Council (EPC). A Marshall Islands IBC using a GB IBAN from such an EMI can send EUR to any bank account in the 36 SEPA member countries. Settlement is typically same-day or T+1. Some EU counterparties may query a GB prefix when initiating a SEPA transfer — in those cases, providing the SWIFT BIC and confirming the issuer's SEPA scheme membership resolves the issue without requiring additional steps.

What documents does a Marshall Islands company need to open a payment account?

Standard documentation for a Marshall Islands IBC onboarding at an FCA-authorised EMI typically includes: certificate of incorporation; memorandum and articles of association; register of directors and shareholders; UBO declaration for all beneficial owners holding 25% or more; proof of business activity (contracts, invoices, or business description); and source of funds documentation (bank statements or audited accounts). Certified copies are generally accepted. Apostilled documents may be required depending on the EMI's KYB policy and the complexity of the IBC's ownership structure. Additional documentation may be requested for structures involving nominees, foundations, or multi-layer holding arrangements.

Is a GB IBAN accepted for SEPA transfers to EU suppliers?

A GB-prefixed IBAN is technically eligible for SEPA Credit Transfer provided the issuing EMI is a SEPA scheme participant. The UK left the EU but several UK-regulated payment institutions retain SEPA scheme membership, enabling them to process EUR transfers across the SEPA zone. For a Marshall Islands IBC using a GB IBAN from such an EMI, outbound SEPA SCT payments to EU suppliers process normally. EU counterparties who query the GB prefix can be given the issuing EMI's BIC and SEPA membership confirmation — standard practice for any cross-border IBAN used post-Brexit.

How to open a GBP EUR account for a Marshall Islands company with a UK EMI

A Marshall Islands IBC opens a GBP EUR account with a UK EMI by submitting an online application with corporate documentation, UBO identification, and source of funds evidence. The EMI conducts digital KYB and, once approved, issues a named GB IBAN and sort code for GBP and a EUR IBAN for SEPA access — both in the IBC's legal name. How Marshall Islands registered IBC gets UK sort code and EUR IBAN without local presence follows this process: there is no requirement to establish a UK branch, appoint a UK director, or visit any office. The process is fully remote, typically completed within 5–10 business days from document submission, subject to KYB review. EQWIRE processes applications from Marshall Islands IBCs through its standard online onboarding at client.eqwire.com/sign-up.

For a Marshall Islands IBC transacting with UK and EU counterparties, a Marshall Islands company GBP EUR account UK through a single FCA-authorised EMI account resolves the primary banking access barrier in a direct and fully regulated way. GBP receipts settle in real time via Faster Payments. EUR payments reach EU suppliers same-day or T+1 via SEPA SCT. The IBC holds both balances separately and converts between currencies on demand.

The solution exists because the Electronic Money Regulations 2011 create a distinct class of regulated payment service providers that can issue UK payment accounts to non-UK entities. This framework is not a gap or a workaround — it is the designed outcome of UK financial regulation. Marshall Islands companies with legitimate trading activity and transparent beneficial ownership are eligible to access this infrastructure through EQWIRE. Applications can be submitted at client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)