•

•

Multi-Currency Account for Caribbean Businesses: Hold XCD, USD and GBP Together

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Correspondent banking relationships across the Caribbean have thinned sharply over the past decade. Many OECS-registered companies now depend on a single USD or GBP correspondent bank, with no backup if that relationship is withdrawn. A supplier payment that should settle in two days can take five, and a single de-risking decision by a global bank can freeze an entire payment channel overnight. For a company trading in Eastern Caribbean Dollars (XCD) locally, invoicing clients in US dollars, and paying UK suppliers in pounds, that fragility multiplies across three currencies and, typically, three separate banking relationships. A multi-currency account Caribbean XCD USD GBP setup addresses this directly: it lets a business hold XCD, USD and GBP balances inside one FCA-regulated account instead of running a local bank, an offshore account and a UK relationship side by side.

[aa key-takeaways]

Key Takeaways

Traditional Caribbean banks handle XCD well but route USD and GBP payments through correspondent banks that are shrinking in number and raising costs.

Most UK EMIs and neobanks support USD and GBP natively but do not extend to XCD, leaving a coverage gap for Caribbean-registered businesses.

The XCD's fixed 2.70-to-1 peg against the US dollar changes how FX risk should be managed compared with a floating currency like GBP.

A single FCA-regulated multi-currency account can replace three separate banking relationships, cutting reconciliation work and conversion fees.

The right setup depends on transaction volume and currency mix, plus how much regulatory protection a business needs for client funds.

[aa btn]Book a Call[/aa]

[/aa]

What Is a Multi-Currency Account and Why the XCD-USD-GBP Mix Matters

A multi-currency account is a single account that holds balances in several currencies without converting them automatically on receipt. A business receiving USD keeps it in USD until it chooses to convert or spend it. This differs from a standard domestic account, which converts every incoming foreign payment immediately, often at an unfavourable rate buried inside the transaction.

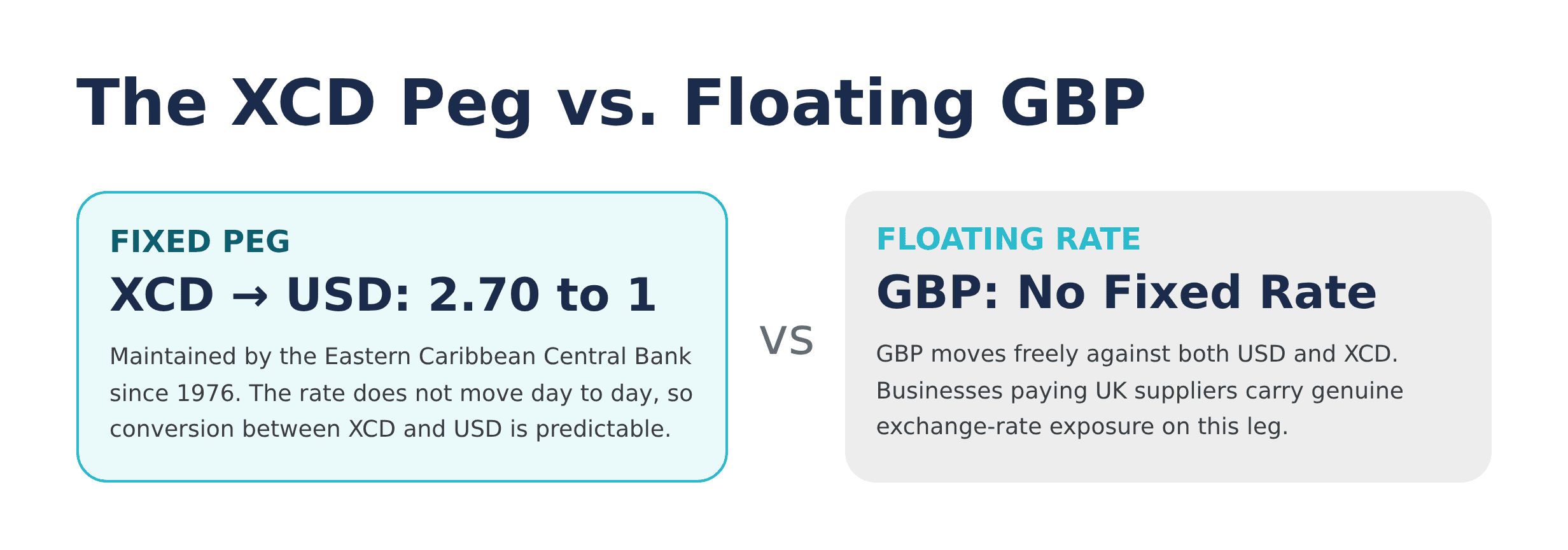

The Eastern Caribbean Central Bank (ECCB) has maintained the XCD at a fixed rate of 2.70 to 1 US dollar since 1976. That peg gives businesses price certainty on the XCD leg of their finances: a supplier quote in XCD converts to USD predictably, with no daily rate movement to track or hedge against.

[aa fast-fact]

Fast Fact: The Eastern Caribbean Dollar has been pegged to the US dollar at a fixed rate of 2.70 to 1 since 1976, maintained by the Eastern Caribbean Central Bank.

[/aa]

GBP behaves differently. It floats freely against both USD and XCD, so a business paying UK suppliers carries genuine exchange-rate exposure that a fixed peg cannot offset. Combining hold XCD, USD and GBP in one account matters precisely because the three currencies carry different risk profiles: one fixed, one reference, one floating.

A SWIFT MT103 message carrying a GBP payment from a UK supplier can pass through two or three correspondent banks before reaching a Caribbean beneficiary account, and each hop can add a working day and a small deduction. Holding GBP natively inside a UK multi-currency account removes several of those hops for outbound and inbound GBP payments, since the funds move on domestic UK rails rather than through a cross-border correspondent chain.

Here's where money is lost in practice. An import-export business collecting XCD from local retail customers, invoicing a US distributor in USD, and paying a UK equipment supplier in GBP typically reconciles three separate ledgers each month. Each conversion between accounts adds a spread on top of any wire fee, and timing mismatches between when XCD arrives and when a GBP payment is due can force a business to convert at a worse rate simply because the calendar demands it.

Import-export businesses, tourism operators collecting deposits in multiple currencies, and regional distributors paying overseas manufacturers are the most common candidates for this setup. Each deals with at least two of the three currencies on a recurring, predictable schedule rather than as one-off transactions. EQWIRE applies the same approach to support less common currencies like the Mauritian rupee, where offshore companies face a comparable coverage gap.

Local Caribbean Bank vs Offshore Account vs UK EMI - Where Does XCD Fit?

Caribbean businesses choosing a banking setup usually weigh three options: a local Caribbean bank, an offshore account, or a UK electronic money institution (EMI). Each handles a Caribbean business account holding XCD, USD and GBP differently, and none of the three is a perfect fit on its own.

What Traditional Caribbean Banks Offer

Local banks in OECS member states handle XCD natively and understand regional compliance requirements well. Their weakness shows up on the USD and GBP side. Wire cut-off times are early, often 10:00 AM for GBP and 3:00 PM for USD, and a payment's arrival date depends on how many correspondent banks the SWIFT message passes through.

Correspondent banking de-risking has reduced many Caribbean banks to a single USD or GBP correspondent relationship. What this means in practice: if that one relationship is terminated, a business can lose USD or GBP wire capability entirely until a replacement correspondent is found, sometimes for weeks at a time.

A regional import business paying a UK-based parts supplier once found its GBP wire rejected mid-month after its bank's sole GBP correspondent ended the relationship. The payment had to be rerouted through a second bank, adding four business days and a fresh set of compliance checks before the supplier saw the funds.

What Offshore Accounts Offer

Offshore accounts, often based in Nevis, the British Virgin Islands, or similar jurisdictions, appeal to Caribbean businesses wanting currency flexibility without being tied to one country's banking system. Account opening for non-resident corporate structures is more involved, and due diligence timelines run longer than either a local bank or a UK EMI.

Deposit protection also varies significantly by jurisdiction. What this means in practice: an offshore account might offer wider currency support on paper, but the regulatory backing behind those balances needs individual verification rather than assumption, unlike an FCA-regulated multi-currency account Caribbean XCD USD GBP structure with a defined safeguarding regime.

What UK EMIs Offer That Traditional Banks Don't

A UK EMI typically issues local account details, such as a GBP sort code and account number, so incoming payments arrive like a domestic transfer over UK payment systems rather than an international wire. Client funds held by an FCA-regulated EMI are safeguarded under UK electronic money regulations, which require relevant funds to be held separately from the firm's own operating capital. Caribbean founders comparing providers often face a decision similar to weighing Wise Business against a dedicated FCA EMI for day-to-day international payments.

Few UK EMIs extend this to XCD. A Caribbean business account holding XCD, USD and GBP together, alongside a regional bank relationship for XCD-specific transactions, is currently the more realistic combination for most OECS-registered companies. What this means in practice: businesses gain fast, safeguarded GBP and USD handling through the EMI while keeping a lighter-weight local relationship purely for XCD.

[aa cta]

Stop Managing Three Banking Relationships

Hold XCD, USD and GBP in one FCA-regulated account instead of juggling a local bank, an offshore provider and a UK banking relationship separately.

[aa btn]Compare Account Options[/aa]

[/aa]

Comparing Multi-Currency Providers for XCD, USD and GBP

A UK EMI account for Caribbean companies is usually judged against three criteria: currency coverage, onboarding speed, and cost per transfer. Local banks win on XCD handling and regional compliance familiarity. UK EMIs win on GBP account details, safeguarding under the UK Electronic Money Regulations, and faster USD/GBP settlement through direct banking rails rather than long correspondent chains.

Criteria | Local Caribbean bank | Offshore account | UK EMI |

|---|---|---|---|

XCD support | Native | Sometimes | Rare |

GBP settlement speed | 2-5 days (correspondent-dependent) | 2-4 days | Often same-day via domestic rails |

Fund safeguarding | National deposit scheme | Varies by jurisdiction | FCA safeguarding rules |

Typical onboarding | 1-2 weeks | 3-6 weeks | Days to 2 weeks |

Onboarding timelines differ by provider type. A local bank account for an established business can take one to two weeks once documents are submitted. A UK EMI account typically opens faster for straightforward corporate structures, though the exact timeline depends on KYB checks for the business's ownership and registration documents, including certificates of incorporation and beneficial-owner identification. An offshore account often takes the longest, since due diligence is more extensive for non-resident structures.

Cost comparisons should include hidden FX markup, not just the advertised transfer fee. What this means in practice: a "free" wire that converts XCD to GBP at a 2% markup often costs more than a paid transfer with a transparent mid-market rate. On a $50,000 monthly GBP payment, a 2% hidden markup costs $1,000 every month, regardless of the wire fee shown at checkout. Businesses comparing providers should ask for the underlying FX rate, not just the headline fee.

Currency coverage should also be checked against the actual currency pairs a business uses, not the total number of currencies a provider advertises. A provider listing 60 supported currencies is not more useful than one supporting 12 if XCD, USD and GBP specifically are not among the natively held balances. What this means in practice: the relevant comparison metric is coverage of the three currencies a Caribbean business actually transacts in, not the size of the provider's overall currency list.

When to Choose One Multi-Currency Account vs Multiple Separate Accounts

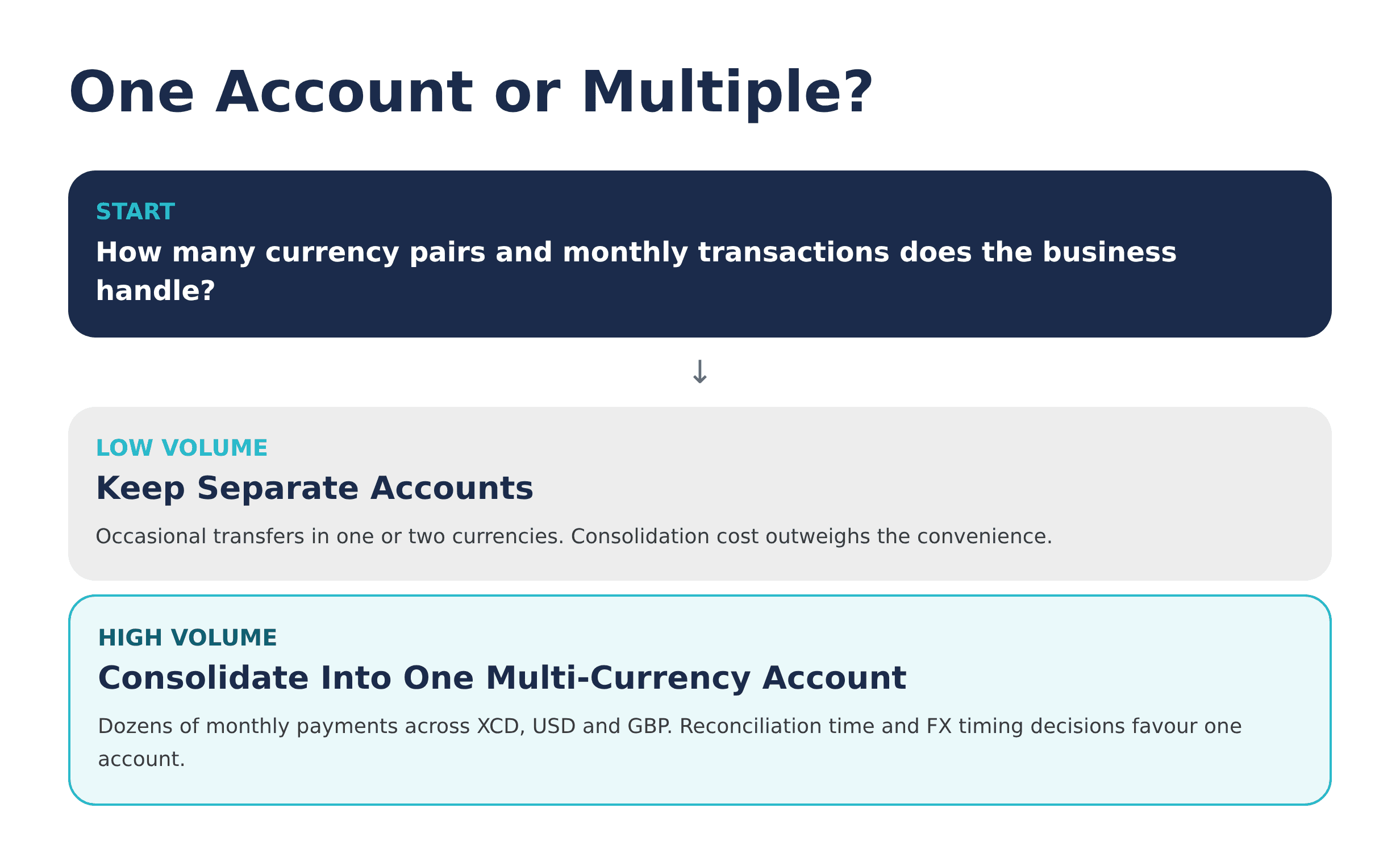

Cross-border payments for SMEs get harder to manage as the number of currencies and counterparties grows, often becoming part of a broader cross-border payments strategy rather than a one-off decision. A business invoicing a handful of US clients each month may manage fine with a local XCD account and occasional wire transfers. A business with dozens of monthly GBP supplier payments and recurring USD client invoices faces a different calculation.

A single XCD USD GBP one account Caribbean business setup makes sense once reconciliation across separate ledgers starts consuming real staff time, or once FX timing decisions need to happen quickly rather than after a multi-day transfer delay. Multiple separate accounts still make sense for businesses with low transaction volume in one or two of the three currencies, where the cost of consolidation outweighs the convenience.

Consider a distribution company that processes 40 GBP supplier invoices and 15 USD client payments each month, alongside daily XCD retail receipts. Before consolidating, its finance team spent roughly six hours a week reconciling three separate statements. After moving USD and GBP into one account, that reconciliation time dropped to under two hours, and the finance team could time GBP conversions around favourable rate windows instead of converting on arrival by default.

What this means in practice: the decision is less about company size and more about transaction frequency and the number of currency pairs actively in use each month. A seasonal tourism business collecting GBP deposits ahead of peak season, for instance, benefits from consolidation even at moderate volume, since deposit timing and payout timing rarely align.

Trade-offs - Cost, Speed and Regulatory Protection

Three factors decide which multi-currency account Caribbean XCD USD GBP setup fits best: cost, speed and regulatory protection. Local banks often cost less per XCD transaction but more per USD or GBP wire once correspondent bank fees stack up. UK EMIs typically charge a transparent FX spread and a flat transfer fee, with faster settlement on GBP payments through domestic rails.

Regulatory protection varies more than businesses expect. Funds held at an FCA-regulated EMI benefit from FCA safeguarding requirements that segregate client money from the firm's operating funds. Offshore accounts vary widely in deposit protection depending on jurisdiction, and local Caribbean banks fall under their own national deposit insurance schemes, which differ from one OECS member state to another. The mechanics of how client funds are ring-fenced under FCA safeguarding rules differ meaningfully from a bank's deposit guarantee scheme.

[aa fast-fact]

Fast Fact: The OECS comprises eight Eastern Caribbean territories, including six independent states and two British Overseas Territories, all sharing the XCD as a common currency.

[/aa]

None of the three options is free of trade-offs. A local bank offers regional trust but slower USD/GBP settlement. An offshore account offers currency flexibility but variable regulatory protection. A UK EMI offers safeguarding and speed on USD/GBP but limited or no native XCD support today. The practical takeaway: most Caribbean businesses get the best outcome from pairing a UK EMI for USD/GBP with a regional bank for XCD, rather than searching for one provider that does all three natively.

Compliance documentation adds a further, often underestimated, layer to this decision. OECS-registered companies typically need a certificate of incorporation, a register of directors and beneficial owners, and proof of trading activity before any provider — local, offshore or UK-based — will approve an account. Gathering these once and reusing them across two providers, rather than three, is itself a meaningful reduction in administrative overhead.

Modelled over a year, the difference compounds. A business paying $2,000 in avoidable correspondent fees and hidden FX markup each month loses roughly $24,000 annually to a fragmented setup, before accounting for staff hours spent reconciling three statements instead of two. The practical takeaway for finance teams building next year's budget is to model total cost of ownership across all three factors together, not the transfer fee in isolation.

[aa cta]

Bring XCD, USD and GBP Into One Account

Open a multi-currency account built for Caribbean businesses trading internationally in Eastern Caribbean Dollars, US dollars and pounds sterling.

[aa btn]Open an Account[/aa]

[/aa]

FAQ

What is a multi-currency account?

A multi-currency account is a single account that holds balances in more than one currency without converting them automatically. Businesses can hold XCD, USD and GBP in one account, choosing when to convert rather than accepting an automatic conversion on every incoming payment. This differs from a standard domestic account, which typically converts foreign receipts immediately at the bank's rate. For companies trading across multiple currencies, this control reduces unnecessary conversion costs and simplifies reconciliation across fewer statements.

How does a Caribbean business open a multi-currency account?

Opening typically starts with KYB documentation required under UK money laundering regulations: certificate of incorporation, proof of registered address, and identification for beneficial owners and directors. Providers assess the business's transaction profile and expected currencies, along with monthly volume, before approving the account. Once approved, the business receives local account details for supported currencies, such as a GBP sort code and account number. Full onboarding for a straightforward corporate structure usually completes within one to two weeks, though timelines vary by provider and by how quickly documentation is submitted.

Can a Caribbean business hold XCD, USD and GBP in one account?

Most UK EMIs and neobanks do not currently extend native support to the Eastern Caribbean Dollar, so an XCD USD GBP one account Caribbean business setup often pairs a UK multi-currency account for USD and GBP with a local or regional bank relationship for XCD-specific transactions. Businesses should confirm XCD availability directly with a provider before onboarding, since coverage changes as providers expand their currency lists. This combination still reduces the number of separate USD and GBP banking relationships a business needs to maintain.

How does a Caribbean business combine XCD, USD and GBP balances in one UK multi-currency account?

A Caribbean business combining XCD, USD and GBP balances in one UK multi-currency account typically holds USD and GBP natively within the UK EMI account, while routing XCD-denominated transactions through a regional banking relationship that feeds into the same reconciliation process. This reduces the account count from three to two in most cases today, with USD and GBP consolidated and XCD handled separately until broader XCD support becomes available. Businesses should treat this as a phased consolidation rather than a single-account solution in the near term.

Is the East Caribbean Dollar pegged to the US dollar?

Yes. The Eastern Caribbean Central Bank has maintained a fixed exchange rate of 2.70 XCD to 1 US dollar since 1976. This peg gives businesses predictable conversion between XCD and USD, unlike the floating rate that applies between XCD and GBP or between USD and GBP. The peg is maintained through the ECCB's monetary policy and foreign exchange interventions, and it has remained stable for nearly five decades.

Combining local banking familiarity with a regulated UK multi-currency account gives Caribbean businesses more control over how XCD, USD and GBP move through the business. The fixed XCD peg simplifies one leg of currency risk, while GBP exposure still requires active management and periodic review. Businesses evaluating a multi-currency account Caribbean XCD USD GBP setup should weigh currency coverage and cost transparency together with regulatory protection, rather than choosing a provider on advertised fees alone. A consolidated account through EQWIRE brings USD and GBP balances into one FCA-regulated relationship, reducing the number of banking relationships a Caribbean business needs to manage day to day and freeing finance teams to focus on growth rather than reconciliation.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)