•

•

How Client Funds Are Safeguarded in a UK FCA EMI Account

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

UK electronic money institutions hold billions in client funds at any given moment. When an EMI fails — and several have, including Wirecard's UK subsidiary in 2020 — the question of what happens to those funds is not theoretical. It is the precise moment when the regulatory framework either works or does not.

For finance teams managing significant payment flows through a UK EMI account, understanding how safeguarded client funds are protected is essential due diligence. This article explains the legal mechanics of FCA safeguarding requirements, what happens to funds in an insolvency event, and how this protection differs from FSCS bank deposit coverage.

[aa key-takeaways]

Key Takeaways

FCA-authorised EMIs are legally required to segregate client funds from their own operational capital under the Payment Services Regulations 2017

Relevant funds — money received from or for the benefit of payment service users — must be safeguarded from the moment of receipt

Two compliant methods exist: segregation into a dedicated account at an approved credit institution, or coverage by an insurance policy or comparable guarantee

Safeguarded client funds are not covered by FSCS, but are ring-fenced by law and returned to clients as priority creditors in insolvency proceedings

Finance teams can verify safeguarding compliance by checking the FCA Register and requesting the EMI's safeguarding documentation before opening an account

[aa btn]Open an Account[/aa]

[/aa]

What Are Safeguarded Client Funds in a UK EMI Account?

When a business sends money to an FCA-authorised EMI — whether for payment execution, e-money issuance, or settlement — that money does not become the EMI's asset. It remains the client's money. The EMI is holding it on behalf of the client, and the law treats it accordingly.

This is the core principle behind safeguarding. Under the Payment Services Regulations 2017 (PSR 2017), FCA-authorised EMIs are legally prohibited from treating client funds as operational capital. They cannot lend it, invest it, or use it to cover running costs.

Understanding the difference between a bank and an FCA-authorised EMI is critical here — because the two operate under different regulatory frameworks, and the protection mechanisms reflect that distinction.

Legal Definition of Relevant Funds Under PSR 2017

The operative term in the safeguarding framework is relevant funds. Regulation 23 of PSR 2017 defines these as funds received from or for the benefit of a payment service user in connection with a payment transaction.

In practice, this means: any money deposited by a client pending a payment instruction, funds held in transit, and amounts received for e-money issuance. The definition is deliberately broad — it covers the full lifecycle of client money held by the EMI.

What is explicitly excluded: the EMI's own capital, fee income already earned and moved to operational accounts, and funds held under separate contractual arrangements that fall outside payment services.

Which Fund Types Are Subject to Safeguarding Obligations

Client funds segregation under EMI FCA rules applies across three primary categories:

Funds pending execution — money received for a payment order not yet processed

E-money float — balances held against issued e-money

Funds in transit — amounts received but not yet delivered to the intended recipient

The distinction matters for businesses holding multi-currency balances. Funds held in a UK payment account across GBP, EUR, and USD are all subject to the same safeguarding obligations, regardless of currency or payment rail.

What this means in practice: every pound sitting in a client balance at an FCA-authorised EMI must be covered by one of the two approved safeguarding methods — from the moment it arrives.

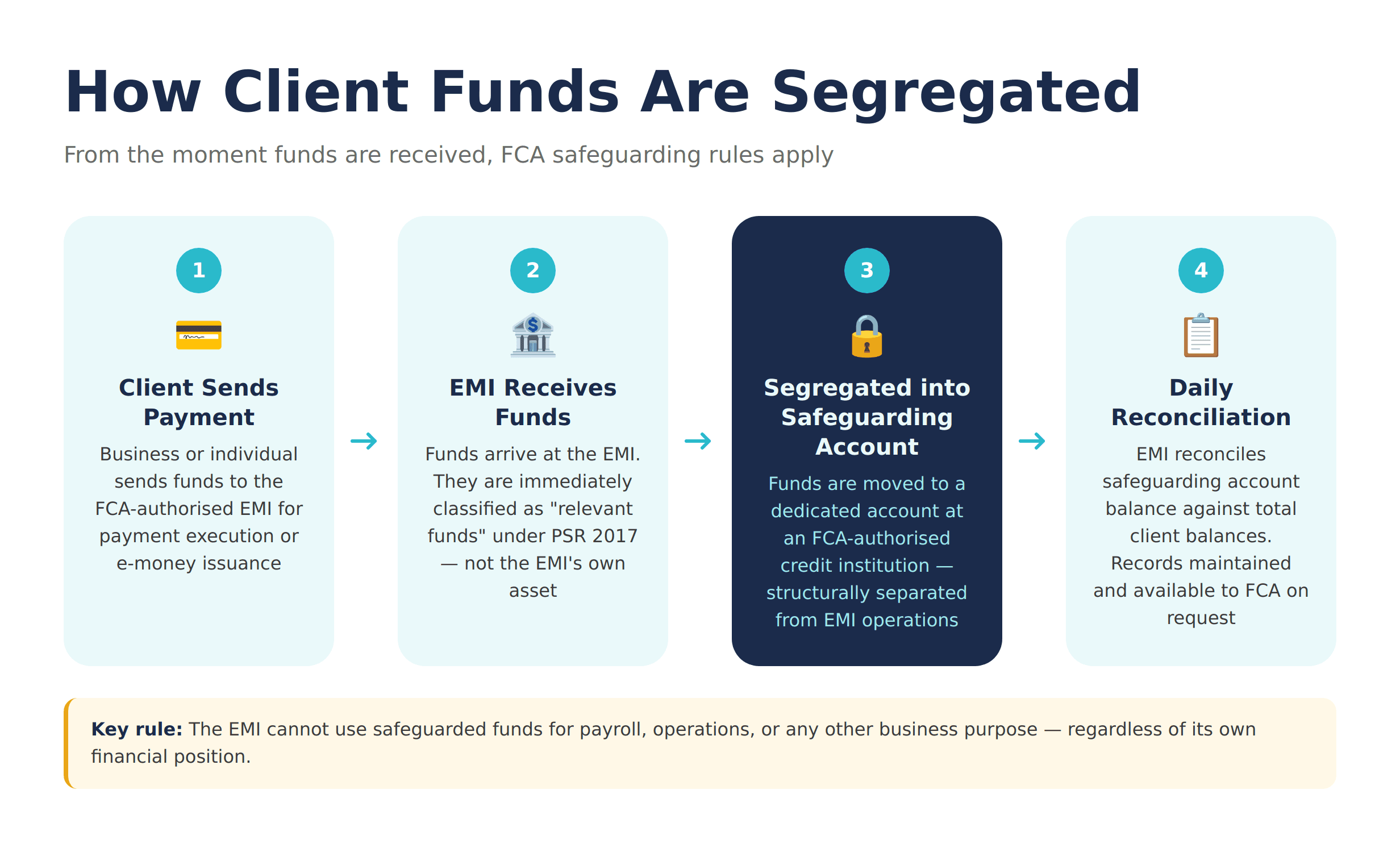

How FCA Rules Require EMIs to Safeguard Client Money

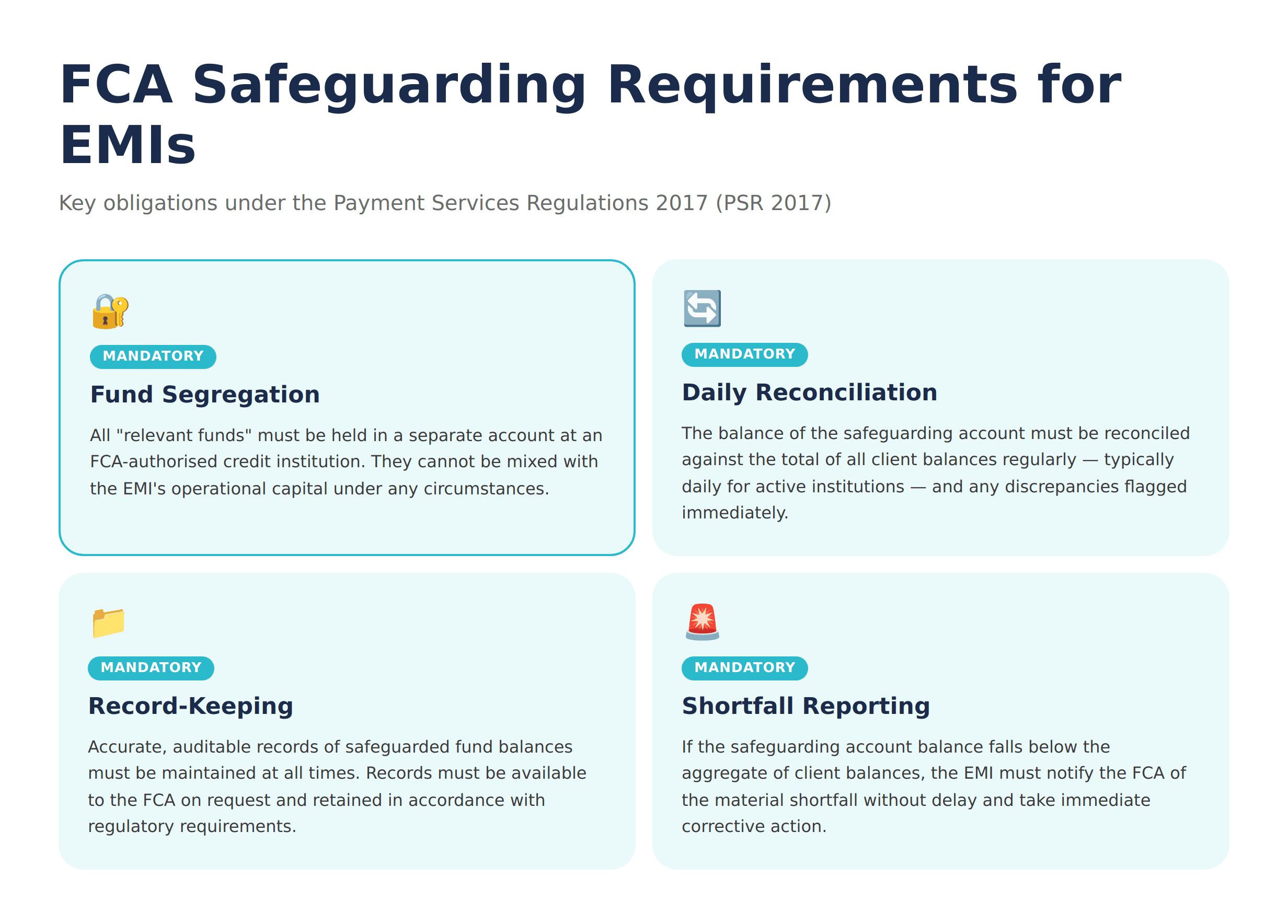

The PSR 2017 specifies two — and only two — methods for how client funds safeguarded in UK EMI accounts can be protected. The EMI must choose one and apply it consistently. There is no discretion to mix methods or apply different approaches to different client segments.

Method 1 — Segregation into a Dedicated Safeguarding Account

This is the most widely used method and the one most finance teams will encounter in practice.

The EMI must place all relevant funds into a separate account held at an FCA-authorised or PRA-regulated credit institution — typically a UK clearing bank. The account must be clearly designated as a safeguarding account in the account title and documentation.

The safeguarding account is structurally walled off from the EMI's own operating accounts. The EMI cannot draw on it to cover payroll, technology costs, or any operational expense. Reconciliation between the safeguarding account balance and the total of client balances must be performed regularly — typically daily for larger institutions.

Method 2 — Insurance Policy or Guarantee

The second permitted approach substitutes insurance for segregation. An insurance policy or comparable guarantee from an authorised insurer or credit institution must cover the full value of relevant funds at all times.

This method is less common. The practical challenge is maintaining a dynamic policy that adjusts in real time as client balances fluctuate. Most EMIs find Method 1 — direct segregation — more operationally straightforward to implement and audit.

Both methods are legally equivalent under PSR 2017. Under either, client funds cannot be used by the EMI and are recoverable in insolvency.

FCA Record-Keeping and Reconciliation Requirements

Here is where the compliance picture becomes granular — and where gaps tend to appear in less rigorous institutions.

The FCA expects EMIs to maintain accurate, up-to-date records of the total value of relevant funds held, the balance in the safeguarding account, and any reconciliation differences. These records must be auditable and available to the FCA on request.

The client money segregation rules for FCA EMI UK business accounts also extend to notifying the FCA of any material shortfall in the safeguarding account.

What this means in practice: a compliant EMI can produce reconciliation records showing — at any point in time — that the safeguarding account balance equals or exceeds the aggregate of all client balances. That is the standard to request.

[aa cta]

Open a UK Business Account with Verified FCA Safeguarding

EQWIRE is an FCA-authorised EMI — client funds are held in a dedicated safeguarding account, fully separated from operational capital.

[aa btn]Open an Account[/aa]

[/aa]

What Happens to Safeguarded Client Funds If an EMI Becomes Insolvent?

A step-by-step understanding of how FCA rules safeguard client funds in UK EMI accounts is only complete when it includes the insolvency scenario. This is what finance teams need to be able to explain to boards, auditors, and risk committees.

The short answer: safeguarded funds are ring-fenced. They are not part of the insolvent estate and cannot be claimed by the EMI's general creditors.

Ring-Fencing in Insolvency — How It Works

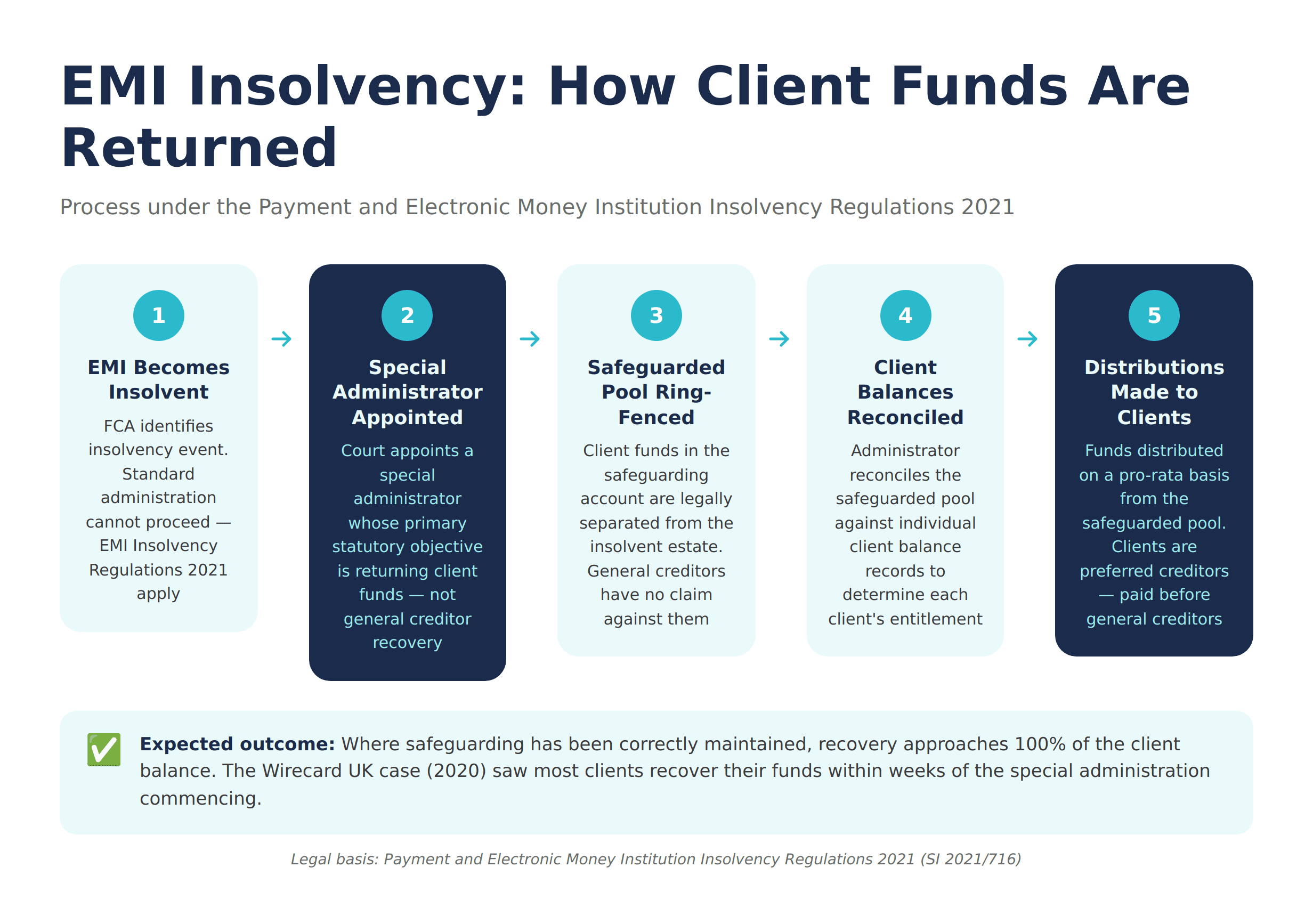

When an FCA-authorised EMI becomes insolvent, the safeguarded fund pool is treated as legally distinct from the EMI's own assets. Suppliers, landlords, lenders, and other creditors of the EMI have no claim against the safeguarded pool.

This ring-fencing is not a contractual protection — it is a statutory one. It exists by operation of law, regardless of what any agreement between the EMI and its creditors says.

Clients become preferred creditors in respect of their safeguarded balances. In a straightforward insolvency, the recovery rate from a properly maintained safeguarded pool is expected to approach 100% of the balance held.

Distribution Process Under the Payment and Electronic Money Institution Insolvency Regulations 2021

The Payment and Electronic Money Institution Insolvency Regulations 2021 (PEMI Regs) created a dedicated special administration regime for insolvent EMIs. A special administrator is appointed — distinct from a standard insolvency practitioner — with a primary objective of returning client funds as quickly as possible.

The distribution sequence is:

Special administrator appointed by court order

Safeguarded pool identified and ring-fenced

Client balances reconciled against the pool

Distributions made to clients on a pro-rata basis from the pool

In the Wirecard UK case, the FCA worked with the appointed administrator to return funds to the majority of affected clients within weeks. The PEMI Regs 2021 were designed to codify and accelerate exactly this process.

The practical takeaway: if safeguarding is correctly maintained, the insolvency of the EMI should not result in permanent loss of client funds. The legal framework is designed for recovery, not write-off.

[aa fast-fact]

Fast Fact: Under the PEMI Regulations 2021, the special administrator's primary objective is the return of client money — not maximising recovery for general creditors. Client funds sit entirely outside the insolvent estate.

[/aa]

Safeguarding vs FSCS Protection — Key Differences

The difference between safeguarding and FSCS protection for UK EMI accounts is one of the most frequently misunderstood aspects of holding business funds at a UK EMI. The two operate on entirely different legal and institutional bases.

Understanding the difference between safeguarding and FSCS protection for UK EMI business accounts begins with a structural fact: EMIs are not deposit-taking institutions.

What FSCS Covers (and Why EMIs Are Excluded)

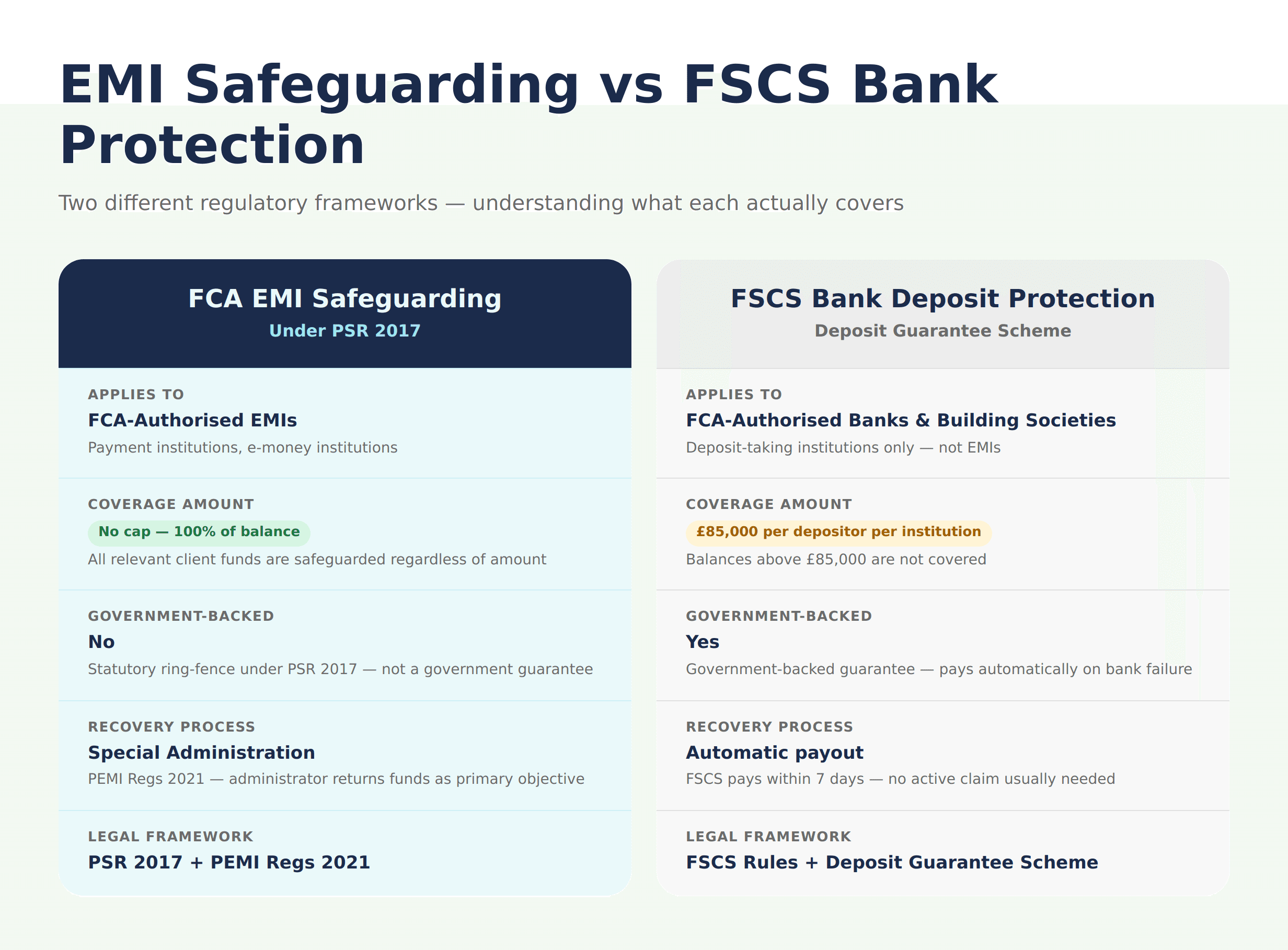

The Financial Services Compensation Scheme (FSCS) protects deposits held at UK-authorised banks and building societies — up to £85,000 per eligible depositor per institution. It is a government-backed guarantee that pays out automatically when a bank fails.

EMIs do not take deposits. They hold money as payment service providers, falling under a different regulatory category. The FCA's guidance on payment institutions confirms that FSCS does not apply to EMIs.

This is not a regulatory gap. It is a deliberate structural distinction. The PSR 2017 safeguarding framework is the equivalent protection mechanism for EMI clients — operating differently, but mandated by law.

Practical Risk Comparison for Business Account Holders

Safeguarded funds protection in a UK EMI account differs from FSCS in three important ways:

Coverage cap: FSCS pays up to £85,000 per institution. EMI safeguarding covers 100% of the relevant fund balance with no upper cap

Government backing: FSCS is a government-backed guarantee. EMI safeguarding is a statutory ring-fence — no government payment, but no cap either

Recovery process: FSCS pays automatically on bank failure. EMI recovery involves special administration under PEMI Regs 2021

For businesses with operational balances consistently above £85,000 — which describes most active SMBs and international operators — the uncapped nature of EMI safeguarding is a meaningful distinction.

Businesses managing cross-border payment flows and international banking through a UK EMI account should factor this into their treasury risk framework, rather than treating the absence of FSCS as a straightforward disadvantage.

How to Verify an EMI's Safeguarding Compliance Before Opening an Account

Understanding how client funds are protected in a UK FCA EMI account is only useful if the specific EMI being evaluated is actually compliant. Regulatory obligation and operational compliance are not the same thing.

The FCA has taken enforcement action against EMIs that failed to meet safeguarding requirements — including issuing requirements notices, imposing restrictions, and in some cases withdrawing authorisation.

Checking FCA Register Status

The first verification step: check the FCA Register.

There are two categories of EMI on the register:

FCA-authorised EMI — fully subject to PSR 2017 safeguarding requirements

FCA-registered (small) EMI — operates under a simplified regime with exemptions from certain PSR obligations, including the full safeguarding framework

For a business holding significant balances, the distinction is material. An FCA-registered EMI is not subject to the same safeguarding requirements as an authorised EMI. The register entry will specify the category — look for Authorised Electronic Money Institution to confirm full PSR coverage.

Businesses receiving client payments into a named IBAN under a UK-regulated account should verify this status before routing significant flows through the account.

Questions to Ask Your EMI About Their Safeguarding Method

Before opening an account, finance teams should request clear answers to these five questions:

Which safeguarding method do you use — bank segregation or insurance/guarantee?

Which FCA-authorised credit institution holds the safeguarding account?

How frequently do you reconcile the safeguarding account against aggregate client balances?

Can you provide the most recent reconciliation confirmation or auditor sign-off?

What is the process for clients to access funds in the event of the EMI's insolvency?

A compliant EMI will answer all five without hesitation. Incomplete or vague responses are a red flag. The standard is clear — and a well-run institution will be familiar with it.

FAQ

How are client funds protected in a UK FCA EMI account?

FCA-authorised EMIs are legally required under PSR 2017 to safeguard client funds by either segregating them into a dedicated account at an FCA-approved credit institution, or covering them with an insurance policy or guarantee. Safeguarded funds cannot be used for the EMI's operational purposes and are ring-fenced in insolvency proceedings, giving clients priority creditor status for recovery.

What does safeguarding mean for business funds in a UK EMI?

Safeguarding means the EMI holds client money separately from its own capital at all times. Business funds deposited with an FCA-authorised EMI are legally classified as relevant funds under PSR 2017 and must be protected from the moment of receipt. The EMI cannot use these funds to cover operational costs, lending, or investment.

What is the difference between safeguarding and FSCS protection for UK EMI business accounts?

FSCS protects deposits at UK banks and building societies up to £85,000 per eligible depositor — it is a government-backed guarantee that does not apply to EMIs. EMI safeguarding is a statutory ring-fence under PSR 2017 that covers 100% of relevant client fund balances with no upper cap. FSCS pays automatically on bank failure; EMI recovery is managed through the special administration regime under the PEMI Regulations 2021.

Client money segregation rules for FCA EMI UK business account — what applies?

Under PSR 2017 Regulation 23, FCA-authorised EMIs must segregate all relevant client funds from their own assets. The segregation account must be held at an FCA-authorised credit institution, designated as a safeguarding account, and reconciled regularly. EMIs are also required to maintain auditable records of the total safeguarded balance and report any material shortfalls to the FCA.

Are business funds safe if a UK FCA EMI becomes insolvent?

If the EMI has correctly maintained its safeguarding obligations, client funds should be recoverable in full. The Payment and Electronic Money Institution Insolvency Regulations 2021 establish a special administration regime with the primary objective of returning safeguarded funds to clients as quickly as possible. Safeguarded funds are ring-fenced from the EMI's insolvency estate and cannot be claimed by general creditors.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)