•

•

MUR to USD or EUR: FX Conversion Options for Mauritius-Based International Businesses

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

Every MUR to USD or EUR FX conversion a Mauritius-based business makes carries a cost that rarely shows up as its own line item. A growing international business registered in Mauritius — including a Global Business Company (GBC) — typically has at least three distinct ways to convert Mauritian rupee into US dollars or euros: a local bank, a multi-currency business account, or a specialised FX/EMI provider.

Each route differs in rate, fees, minimum transfer size, and settlement time. Picking the wrong one quietly erodes margin on every transaction, all year. A trading company that receives MUR from local clients and pays overseas suppliers in USD, for instance, can lose several percentage points twice over — once converting in, once converting out — without ever seeing a separate "FX fee" line.

This guide compares the three routes side by side, explains when a local bank still makes sense, and shows how to calculate the real cost of a MUR conversion beyond the rate printed on a screen.

[aa key-takeaways]

Key Takeaways

Three main routes exist for MUR to USD or EUR FX conversion: local bank, multi-currency account, and specialised FX/EMI provider

Bank of Mauritius indicative rates are the benchmark for spotting hidden markup, not the rate a business should expect to receive

Multi-currency accounts reduce how often a business needs to convert MUR at all

GBC substance requirements shape — but do not lock in — where a business holds its operating currency

The advertised commission is rarely the full cost; the spread against the mid-market rate usually matters more

[aa btn]Book a Call[/aa]

[/aa]

Three Ways to Convert MUR to USD or EUR

Businesses converting Mauritius rupee to USD or EUR through a business account generally choose between three structurally different paths. Each suits a different transaction pattern, and most businesses end up using more than one at different points in their growth.

Local Bank in Mauritius

MCB, SBM, MauBank, and AfrAsia Bank all offer FX conversion for business accounts, quoting a rate derived from — but wider than — the Bank of Mauritius consolidated indicative exchange rate. Execution is often branch-dependent: a relationship manager confirms the final rate before the transaction is booked, and rates can vary between branches of the same bank on the same day.

For a business that converts MUR occasionally — a handful of times a year, in modest amounts — this is usually the path of least resistance. The account already exists, the process is familiar, and the spread on a small, one-off transfer rarely justifies opening a new relationship elsewhere.

[aa fast-fact]

Fast Fact: Bank of Mauritius indicative rates are simple averages submitted by all banks — they show the wholesale reference point, not what any single bank will actually give a business on a live conversion.

[/aa]

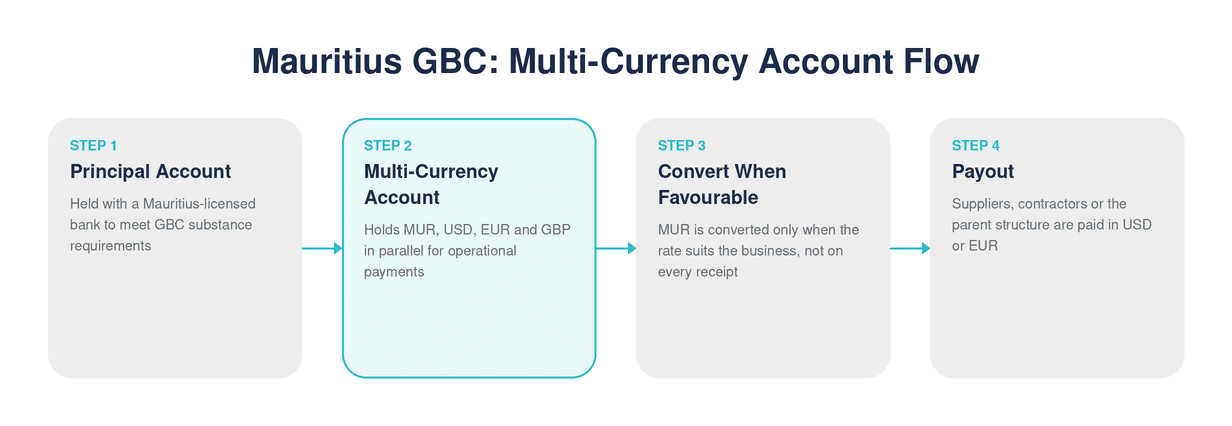

Multi-Currency Business Account

A multi-currency account holds MUR alongside USD, EUR, and GBP in segregated balances under one account structure. Instead of converting every incoming MUR receipt immediately, a business can hold the currency and convert only when the rate is favourable, or receive USD/EUR payments directly without ever touching MUR. A Mauritius GBC can structure its multi-currency account to match its actual mix of receipts and payables.

This matters most for businesses with recurring flows in both directions. Consider an e-commerce seller collecting MUR from local marketplace payouts while paying USD suppliers each month.

Instead of converting MUR to USD on arrival, the business holds both currencies in the same account. It nets the two flows against each other and converts only the difference.

The result: fewer conversions overall, and the ones that still happen are timed by choice rather than forced by an incoming payment. A business expecting to pay a USD invoice in three weeks can receive MUR now, hold it briefly, and convert once the rate looks favourable.

Specialised FX/EMI Provider

Electronic Money Institutions — a regulatory category defined under frameworks such as the UK's e-money regime — and dedicated FX providers typically quote tighter spreads than retail banks on larger or recurring transfers, since their pricing is not bundled with retail banking overhead. Onboarding usually takes longer than opening a standard bank account, because compliance checks are run upfront rather than case by case.

Some providers also let a business receive multi-currency payouts without forced conversion at the point funds arrive, removing one full conversion step from the chain entirely.

Comparing Rate, Fees and Settlement Speed

The three routes for Mauritius business MUR to USD conversion differ most sharply on spread and settlement time, not on the headline commission a provider advertises.

Comparison Table of Conversion Methods

Method | Typical spread vs. mid-market | Fixed fees | Minimum amount | Settlement time |

|---|---|---|---|---|

Local bank in Mauritius | 1.5%–3.5% | MUR 0–500 per transfer | Often none for small amounts | Same day to T+1 |

Multi-currency business account | 0.3%–1% | Low or none on FX | Varies by provider | Instant to T+1 |

Specialised FX/EMI provider | 0.2%–0.8% | Low or none | Sometimes higher minimums | T+0 to T+2 |

What this means in practice: on a MUR 2,000,000 transfer, the difference between a 3% bank spread and a 0.5% provider spread is roughly MUR 50,000 — money that never needed to leave the business.

When a Local Bank Is the Right Choice — and When It Isn't

A local bank is often fine for a one-off, small conversion where convenience outweighs a few percentage points of spread — paying a single local supplier invoice in MUR that happens to originate from a USD receipt, for example.

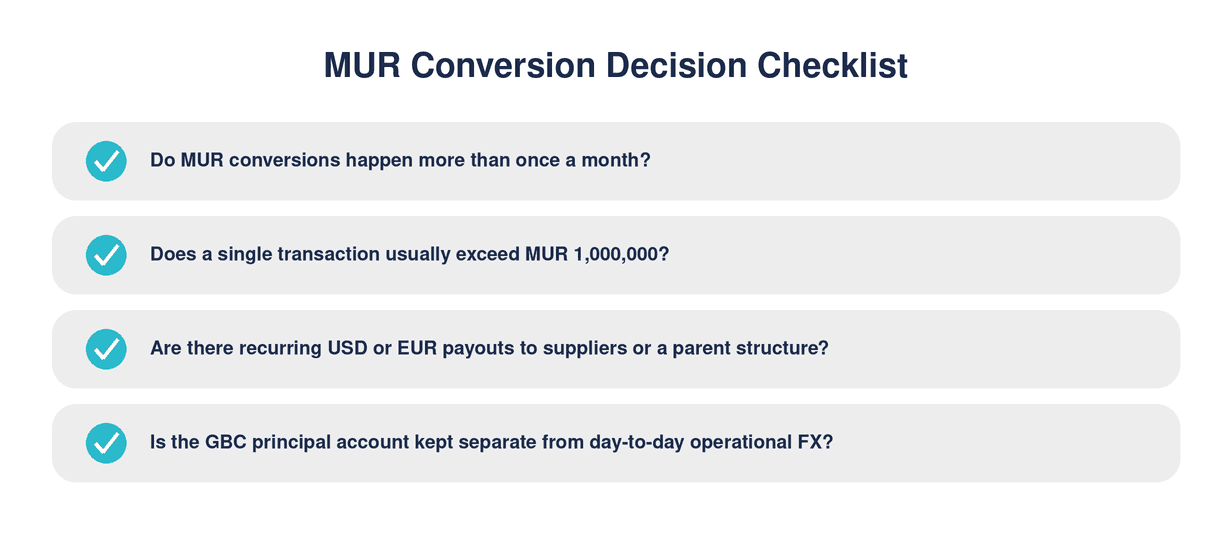

For recurring or larger MUR to USD conversion — monthly payroll to overseas contractors, quarterly dividend repatriation, or supplier payments in EUR — the same spread compounds every cycle. A business converting MUR 5,000,000 a month at a 3% bank spread loses roughly MUR 1,800,000 a year compared with a 0.5% spread elsewhere.

Decision trigger: if MUR conversions happen more than once a month, or exceed roughly MUR 1,000,000 per transaction, the spread difference between a bank and a specialised provider is worth comparing directly rather than assumed.

How a Mauritius GBC Structure Affects the Best Conversion Route

A Global Business Company must maintain its principal bank account with a Mauritius-licensed bank as part of its substance requirements. That does not mean every conversion has to happen inside that account.

Many GBCs keep the principal account for statutory and substance purposes while routing day-to-day USD/EUR payouts, supplier payments, or client collections through a parallel multi-currency account. The principal account satisfies the regulatory requirement; the multi-currency account handles the operational FX exposure at a tighter spread.

[aa fast-fact]

Fast Fact: Mauritius was not on the FATF grey or black list as of mid-2026, which keeps standard due-diligence timelines applicable to most GBC banking relationships rather than enhanced monitoring.

[/aa]

Preparing to Move Recurring Conversions Away from a Bank

Switching some or all of a business's MUR conversions away from a single bank is mostly an administrative exercise, not a technical one, but it goes faster with the right preparation.

Documentation for a Multi-Currency Account

Most providers ask for the same core set of documents as a bank: certificate of incorporation, register of directors and shareholders, proof of business address, and identification for ultimate beneficial owners. GBCs typically also need to show the licence or authorisation issued by the Financial Services Commission.

Migrating Recurring Payments Without Disruption

A practical approach is to run both channels in parallel for one full payment cycle — leave existing bank-based payroll or supplier payments as they are, and route only new or renegotiated payments through the new account. This avoids disrupting a supplier or employee mid-cycle while the new setup is tested against real transaction volumes.

How to Calculate the Real Cost of Converting MUR

The rate quoted on a screen is rarely the full story behind converting Mauritius rupee to USD or EUR through a business account.

Hidden Spread vs. Advertised Commission

A bank might advertise "no transfer fee" while building its margin entirely into the exchange rate — a spread of 2%–3% against the Bank of Mauritius indicative rate is common and easy to miss if a business only checks the commission line.

To find the real cost: compare the rate actually applied to the transaction against the Bank of Mauritius indicative rate published the same day, then multiply the percentage difference by the transaction size. That figure — not the advertised fee — is what a business is actually paying.

Worked example: a business converting MUR 3,000,000 to USD, where the Bank of Mauritius indicative rate implies MUR 46.80 per USD but the bank applies MUR 48.20, is paying roughly a 3% spread — around MUR 90,000 lost on that single transaction, with zero fee shown on the statement.

[aa cta]

See Your Real MUR Conversion Cost

Open a multi-currency account and convert MUR to USD or EUR at a transparent, published rate.

[aa btn]Open a Multi-Currency Account[/aa]

[/aa]

How international businesses operating in Mauritius convert MUR to USD or EUR efficiently ultimately comes down to matching the conversion method to transaction frequency and size, then checking the actual spread against the Bank of Mauritius benchmark on every transfer that matters.

The same hidden-markup dynamic applies to other emerging-market currency pairs businesses manage alongside MUR, such as AED to GBP conversions or HKD to GBP transfers — the spread, not the fee, tends to be where money is actually lost.

Cross-border correspondent banking chains, which many bank-routed MUR to USD or EUR FX conversion payments still pass through, add cost and delay at each intermediary step — a pattern the Bank for International Settlements has documented globally as a structural driver of higher fees on emerging-market currency routes. Regulatory attention on the same issue, including from the Bank of England's work on cross-border payments, points to the same conclusion: fewer intermediaries in the payment chain generally means a tighter spread and a faster settlement.

[aa cta]

Stop Losing Margin on Every MUR Conversion

Hold MUR, USD and EUR in one account and convert only when the rate works for you.

[aa btn]Get Started[/aa]

[/aa]

FAQ

How do international businesses operating in Mauritius convert MUR to USD or EUR efficiently?

Most efficient conversions combine a multi-currency account to hold MUR, USD and EUR without forced conversion, with occasional use of a specialised FX/EMI provider for larger transfers. Comparing the applied rate against the Bank of Mauritius indicative rate on the day of conversion is the fastest way to confirm efficiency.

Which conversion method is cheapest for Mauritius business MUR to USD conversion?

For recurring or larger transfers, a multi-currency account or specialised FX/EMI provider is typically cheaper than a local bank, with spreads around 0.2%–1% against the mid-market rate compared with 1.5%–3.5% at retail banks. For a single small transaction, a local bank's convenience can outweigh the marginal spread difference.

Is a multi-currency account suitable for a Mauritius GBC structure?

Yes. A GBC must keep its principal bank account with a Mauritius-licensed bank for substance purposes, but it can run a parallel multi-currency account for day-to-day USD, EUR, and GBP transactions, separating regulatory compliance from operational FX cost.

How can a business compare the real cost of MUR conversion between providers?

Compare the rate each provider actually applies against the Bank of Mauritius indicative rate published the same day, not against the provider's own advertised rate. The percentage difference, multiplied by the transaction size, shows the true cost.

Do businesses need to switch banks if their current MUR conversion rate is unfavourable?

Not necessarily. A business can keep its existing bank relationship for statutory or local payment needs while routing recurring USD/EUR conversions through a multi-currency account or FX/EMI provider that offers a tighter spread.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)