•

•

Mauritius Global Business Company (GBC): Multi-Currency Account Options

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A newly licensed Global Business Company in Mauritius often needs to do three things in its first month: receive USD from clients, pay EUR suppliers, and hold Mauritian rupees for local costs. The banking setup that supports all three is narrower than most founders expect. In practice, a Mauritius GBC multi-currency account holding MUR, GBP, EUR and USD is rarely a single product. It is usually two accounts working together: the principal bank account that the company must keep in Mauritius, and a UK Electronic Money Institution (EMI) account that adds fast access to major currencies. This guide explains which currencies sit where, the documents each provider asks for, realistic onboarding timelines, and the mistakes that delay applications.

[aa key-takeaways]

Key Takeaways

A GBC must keep its principal bank account in Mauritius to satisfy the Financial Services Commission's substance test. This account anchors MUR and local operations.

Most GBCs run a two-account structure: the mandatory Mauritius account plus a UK EMI account for GBP, EUR and USD.

Mauritius has no foreign-exchange controls, so a GBC can move funds in and out across currencies freely.

Opening a UK EMI account as an offshore company requires enhanced due diligence, including a structure chart, UBO declaration, and source-of-funds evidence.

Local bank onboarding typically takes weeks; a UK EMI account can often open in days once documents are clean.

A UK EMI account complements the local account. It does not remove the requirement to bank in Mauritius.

[aa btn]Book a Call[/aa]

[/aa]

The Multi-Currency Setup a Mauritius GBC Actually Needs

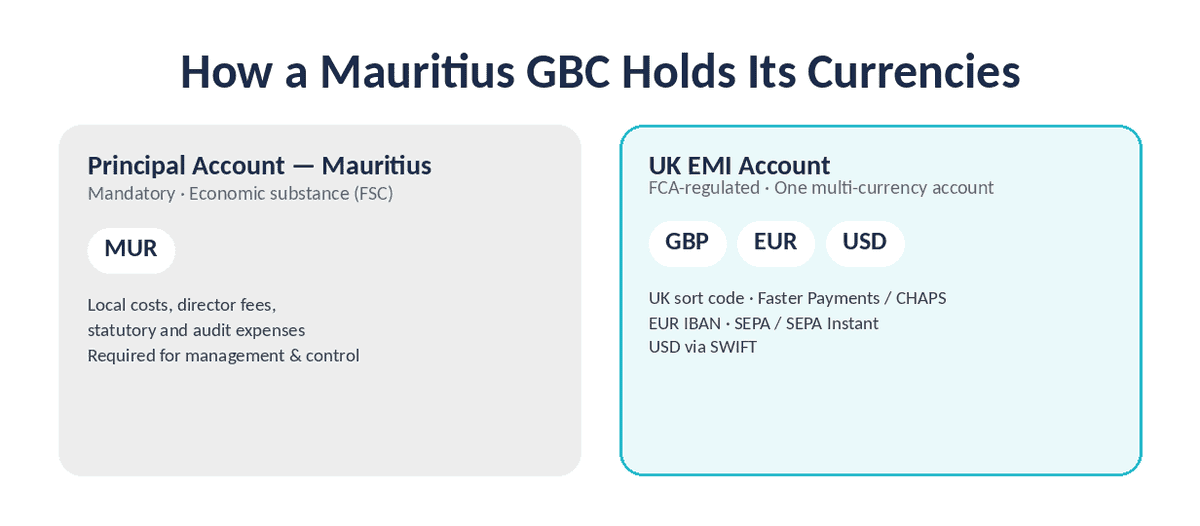

A Mauritius GBC must keep its principal bank account in Mauritius, where it can hold MUR alongside USD, EUR and GBP. That single rule shapes every currency decision the company makes. The realistic answer to "where do we hold each currency" is a two-layer setup: a local account for substance and rupee operations, and a separate account for high-volume major-currency flows.

The reason is practical. A local Mauritian account satisfies regulation and holds MUR well, yet its international transfers can be slower and pricier than businesses trading with EU and US counterparties want. A second account on UK and EU payment rails fills that gap.

Layer 1: The Mandatory Principal Account in Mauritius

The principal account is not optional. When the Financial Services Commission assesses whether a GBC is managed and controlled from Mauritius, one factor it weighs is whether the company maintains its principal bank account on the island. The same substance framework expects at least two resident directors, accounting records kept locally, and financial statements audited in Mauritius.

This account typically holds MUR for local expenses, director fees, and statutory costs. Mauritian banks such as MauBank, AfrAsia, and MCB also offer foreign-currency accounts in USD, EUR, GBP, and others, so a GBC can receive major currencies here too. Offshore companies that want to receive Mauritian rupees without a domestic banking relationship can also hold the Mauritian rupee without a local bank through a specialist provider, though the substance account itself stays in Mauritius.

Local banks scrutinise the trade story behind a GBC before opening. Reviewers want to see who the company sells to, who it pays, and where its income originates. A foreign-currency receipt into a Mauritian account often clears through correspondent banks, which can add a day or two and an intermediary fee to each USD or EUR transfer. That cost is acceptable for occasional movements. It becomes a drag once a GBC processes dozens of cross-border payments a month, which is where the second layer earns its place.

Layer 2: A UK EMI Account for GBP, EUR and USD

The second layer is a UK Electronic Money Institution account. An EMI is authorised to issue electronic money and provide payment services, and it can offer multi-currency accounts with local payment details. EQWIRE, for example, is a UK EMI authorised and regulated by the Financial Conduct Authority under firm reference number 901100, which can be checked on the FCA's Financial Services Register.

An EMI account gives a GBC GBP with a UK sort code, EUR with an IBAN, and USD, all reachable from one login. Funds are safeguarded under the Electronic Money Regulations 2011 rather than covered by the Financial Services Compensation Scheme, a distinction every applicant should understand before opening. For a fuller view of how this option compares to other providers, see how an FCA-regulated EMI compares for offshore companies.

The speed advantage comes from the rails an EMI plugs into directly. A GBP balance reaches the UK Faster Payments system, where most transfers settle in seconds. A EUR balance sits on SEPA, so payments to EU suppliers clear the next business day or, on SEPA Instant, in under ten seconds. Holding these currencies natively also means a GBC converts only when it chooses to, instead of paying a conversion cost on every inbound receipt. That control over timing is the main reason trading companies add an EMI account rather than routing everything through the local bank.

Matching Currencies to Accounts (MUR, GBP, EUR, USD)

Each currency has a natural home. MUR belongs in the Mauritius account, where local costs and statutory obligations are paid. GBP, EUR, and USD generally flow more efficiently through a UK EMI account on dedicated rails.

The split keeps the substance account clean for compliance while routing trade receipts and supplier payments through faster channels. A GBC foreign currency account on the EMI side becomes the working account for cross-border business.

The table below shows where each currency usually sits and why.

Currency | Primary home | Main rail | Why it sits there |

|---|---|---|---|

MUR | Mauritius principal account | Local clearing | Local costs, director fees, statutory and audit expenses |

GBP | UK EMI account | Faster Payments / CHAPS | UK sort code, settlement in seconds to same day |

EUR | UK EMI account | SEPA / SEPA Instant | IBAN, next-day or sub-10-second settlement to the EU |

USD | UK EMI account | SWIFT | Global reach for US and dollar-invoiced clients |

The point of the map is not to move every balance offshore. It is to put each currency on the rail that handles it best, while the Mauritius account keeps doing the compliance job only it can do.

[aa fast-fact]

Fast Fact: Mauritius applies no foreign-exchange controls, so a GBC can transfer funds in and out of the country and convert between MUR, GBP, EUR and USD without regulatory caps on movement.

[/aa]

How to Open Multi-Currency Accounts for a GBC, Step by Step

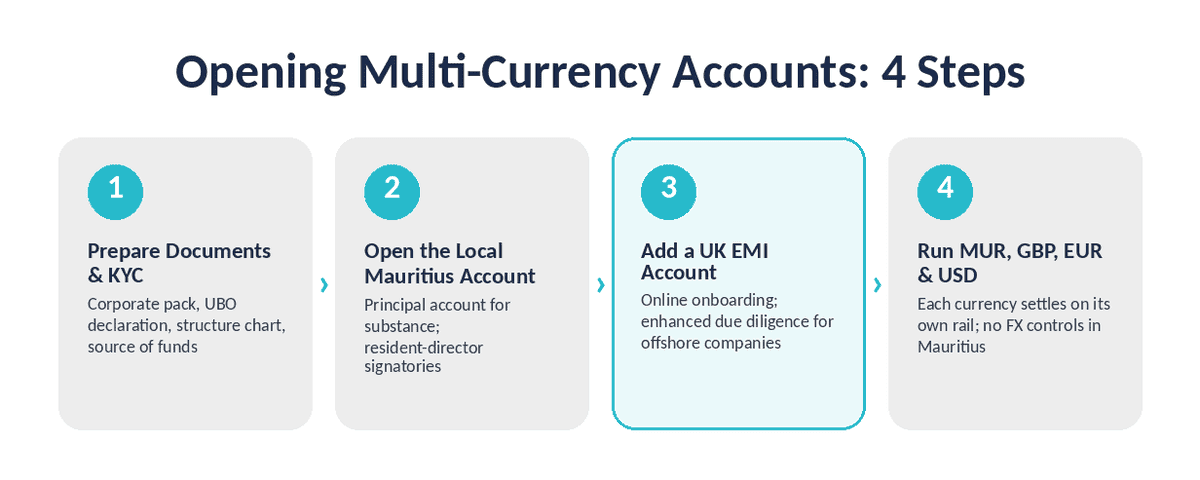

Knowing how to open a multi-currency account for a Mauritius GBC means working two tracks in sequence: the mandatory local bank account first, then the UK EMI account. The documents overlap, so preparing one set early speeds up both.

Step 1: Prepare the Documents and KYC a GBC Must Provide

The documents to open a Mauritius GBC bank account start with the corporate pack: certificate of incorporation, the Global Business Licence, the constitution, and a register of directors and shareholders. Providers then run know-your-customer and anti-money-laundering checks on the people behind the company.

A typical document set for both the local account and the EMI account includes:

Certificate of incorporation and the Global Business Licence

Company constitution and register of directors and shareholders

Proof of registered office and the company's principal address

Passport copies and proof of address for each director and beneficial owner

A UBO declaration and a corporate structure chart

A description of the business, expected currencies, and payment volumes

Source-of-funds and source-of-wealth evidence

Offshore structures attract closer scrutiny. Expect enhanced due diligence: a corporate structure chart, an ultimate beneficial owner (UBO) declaration, proof of address for directors and owners, and evidence of source of funds. A clear business description matters as much as the paperwork, because reviewers need to understand the trade flows behind the account. The AML and KYC checks an offshore company should expect are worth reviewing before applying.

Step 2: Open the Local Mauritius Bank Account

The principal account comes first because it underpins the company's substance. The management company or registered agent usually coordinates this with a local bank, submitting the corporate pack and KYC files.

Resident directors and the management company should hold signatory power over the account, since the FSC expects signatory rights not to sit solely with the client. Banks review the file, may request clarifications, and then open MUR and foreign-currency sub-accounts.

Step 3: Add a UK EMI Multi-Currency Account

With the company verified, the offshore company UK EMI account is the next step. Most EMIs run onboarding online, so the GBC uploads the same corporate and UBO documents and answers questions about expected currencies and volumes.

Once approved, the account issues GBP details with a UK sort code, a EUR IBAN, and USD access. A GBC can then open a GBP account with a UK sort code for a non-UK company and start receiving payments on local rails rather than through correspondent chains.

Step 4: Expect Realistic Timelines at Each Stage

Timelines differ sharply between the two tracks. Local Mauritian bank onboarding often runs several weeks, because corporate reviews and substance checks take time.

A UK EMI account usually opens faster, in days rather than weeks, once enhanced due diligence is satisfied and documents are clean. Incomplete files are the single biggest cause of delay on either track.

[aa cta]

Hold GBP, EUR and USD for Your GBC in One Place

A UK EMI account lets a Mauritius GBC receive and send major currencies on local rails, working alongside the principal account in Mauritius.

[aa btn]Open a Business Account[/aa]

[/aa]

Common Mistakes That Delay GBC Currency Accounts

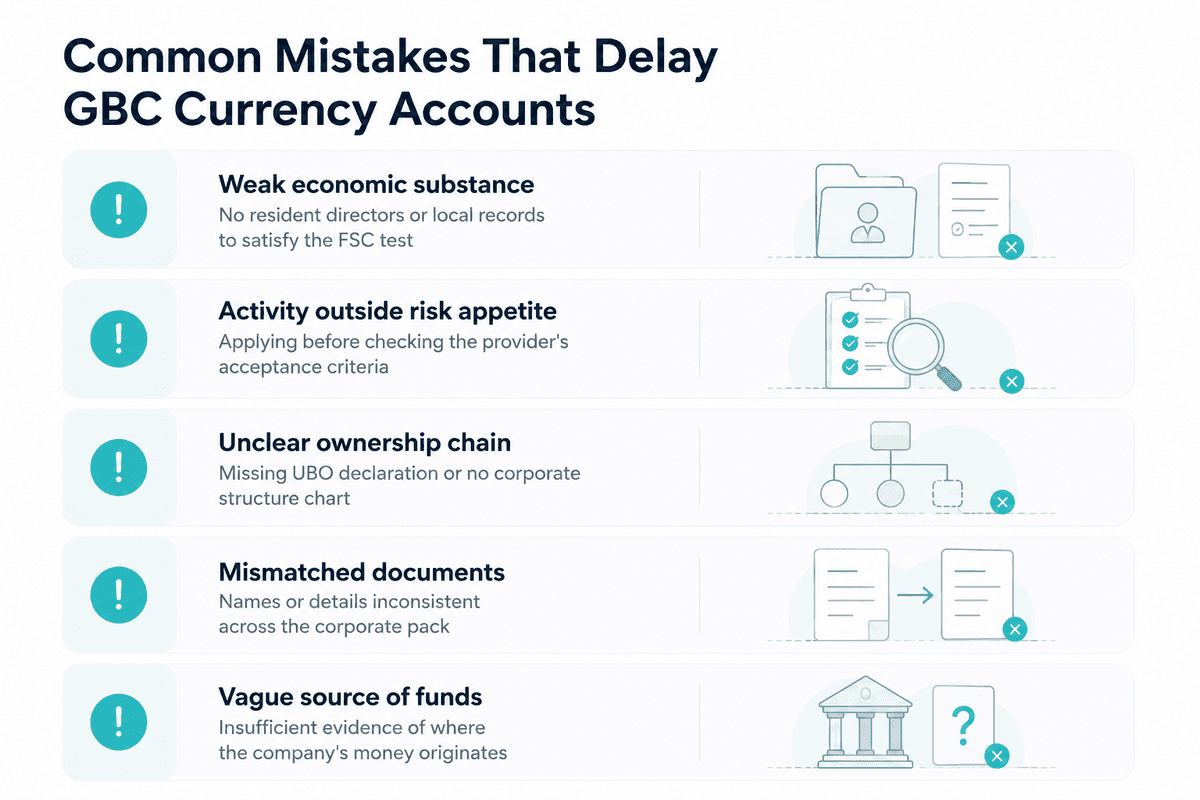

Most rejected or stalled applications fail for predictable reasons. A Mauritius GBC account with MUR, GBP, EUR and USD across the local bank and a UK EMI clears faster when the company avoids two recurring problems.

Substance and Eligibility Gaps

The first is weak substance. If a GBC cannot show resident directors, local records, or a credible reason to bank in Mauritius, reviewers question the structure. Eligibility gaps also matter on the EMI side, where certain jurisdictions and business activities fall outside a provider's risk appetite.

Activity type is the quiet dealbreaker. A provider that serves trading and service companies may still decline sectors it treats as high risk, and a GBC that applies without checking acceptance criteria loses days to a predictable rejection. Confirming both substance and activity fit before applying removes most of these failures at the source.

Documentation and Structure Errors

The second is messy documentation. Mismatched names across documents, an unclear ownership chain, missing UBO declarations, or vague source-of-funds evidence all trigger requests for more information, and each round adds days or weeks.

Ownership chains cause the most friction. When a GBC sits under a holding company or a trust, reviewers need to trace control all the way to the natural persons who own it. A structure chart that names every entity and every percentage answers that question before it is asked. A complete, consistent file submitted once is the fastest route to a live account.

Running MUR, GBP, EUR and USD Day to Day

Once both accounts are live, the day-to-day pattern is straightforward. The Mauritius account holds MUR and covers local obligations. The UK EMI account handles GBP, EUR, and USD trade flows, with each currency settling on its own rail.

GBP moves through Faster Payments and CHAPS for same-day settlement, EUR runs on SEPA and SEPA Instant, and USD typically routes via SWIFT. Because Mauritius applies no exchange controls, the company can repatriate funds to the local account or convert between currencies as trade requires. A GBC that trades across several corridors can manage receivables and payables across currencies from the EMI account, keeping the substance account focused on local compliance.

Consider a GBC that consults for clients in London and Frankfurt and pays a contractor in the United States. It invoices the London client in GBP and receives the payment into its UK sort code the same day. The Frankfurt client pays in EUR, arriving by SEPA the next morning. The contractor is paid in USD over SWIFT, while MUR stays in the Mauritius account to cover the audit fee and resident-director costs. One currency setup, four jobs, no second local banking relationship required.

The result is a clean division of labour. The Mauritius account proves the company is managed and controlled on the island, and the EMI account does the daily work of receiving and sending major currencies. That structure scales as volumes grow, because adding a new corridor means using an existing rail rather than opening another bank account.

FAQ

What currency accounts can a Mauritius Global Business Company hold in a UK EMI?

A Mauritius Global Business Company can hold GBP, EUR, and USD accounts in a UK EMI, usually alongside several other major currencies in one multi-currency account. The GBP balance comes with a UK sort code and Faster Payments access, the EUR balance with an IBAN on SEPA, and USD through SWIFT. These sit in addition to the company's principal bank account in Mauritius, not in place of it. The EMI account is authorised and supervised by the Financial Conduct Authority, and client funds are safeguarded under the Electronic Money Regulations 2011 rather than covered by the FSCS.

What documents does a Mauritius GBC need to open a multi-currency account?

The documents to open a Mauritius GBC bank account include the certificate of incorporation, the Global Business Licence, the company constitution, and a register of directors and shareholders. Providers also require know-your-customer files for directors and beneficial owners, a UBO declaration, proof of address, and evidence of source of funds. Offshore companies should expect enhanced due diligence, including a corporate structure chart and a clear description of the business and its trade flows.

How long does it take to open a GBC account with a UK EMI?

A UK EMI account for a Mauritius GBC typically opens within days once enhanced due diligence is complete and the documents are consistent. This is usually faster than the local Mauritian bank account, which can take several weeks because of corporate and substance reviews. The main variable is document quality: incomplete or mismatched files extend the timeline on both tracks.

Can a Mauritius GBC hold MUR, GBP, EUR and USD across two accounts?

Yes. Most GBCs hold MUR in the principal account in Mauritius and hold GBP, EUR, and USD in a UK EMI account. This split keeps the substance account aligned with Financial Services Commission expectations while routing major-currency trade flows through faster UK and EU rails. The two accounts operate together, giving the company full coverage across all four currencies.

Does a UK EMI account remove the need for a Mauritius bank account?

No. A UK EMI account complements the principal account but does not replace it. The FSC's substance framework expects a GBC to maintain its principal bank account in Mauritius, so the local account remains mandatory. The EMI account adds speed and reach for GBP, EUR, and USD, while the Mauritius account anchors the company's local presence and MUR operations.

A Mauritius GBC multi-currency account holding MUR, GBP, EUR and USD comes together as two coordinated accounts rather than one. The principal account in Mauritius satisfies the substance requirement and runs local operations, while a UK FCA-regulated EMI account gives the company fast, low-friction access to major currencies on dedicated payment rails. Getting the documents right the first time, mapping each currency to the right account, and understanding how safeguarding differs from deposit protection are the steps that keep onboarding on schedule. For GBCs trading across borders, that combined setup turns currency handling from a monthly obstacle into routine operations.

[aa cta]

One Account for All Your International Business Payments

Open an EQWIRE business account to hold and move GBP, EUR, USD and more alongside your Mauritius GBC's local bank account.

[aa btn]Open Business Account[/aa]

[/aa]

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)