•

•

UK Business Account for Panama Company: GBP and EUR Without a Panama Bank

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A Panama company can sign UK and EU clients in a week and still wait months for a way to get paid. Panamanian banks rarely issue usable GBP or EUR rails to non-resident-facing entities, and many European banks now refuse funds that originate from a Panama bank account. The result is a working business with invoices it cannot collect. There is a regulated route around this. A Panama company UK business account for GBP and EUR can be opened through a UK FCA-authorised electronic money institution (EMI), with no Panama bank involved. The account provides a real UK sort code and account number plus a EUR IBAN. This guide covers eligibility, the documents to prepare, the step-by-step setup, and the rejection traps that catch offshore applicants.

[aa key-takeaways]

Key Takeaways

A Panama company can hold GBP and EUR through a UK FCA-authorised EMI, with no Panama bank account involved.

The account delivers a genuine UK sort code and account number for GBP, plus a EUR IBAN for SEPA payments.

Funds are safeguarded under the Electronic Money Regulations 2011, not covered by the FSCS. The protection model differs from a high-street bank.

Eligibility turns on ownership transparency, business activity, and KYB documentation, not on the Panama jurisdiction by itself.

Most rejections trace back to fixable gaps: vague activity descriptions, an incomplete ownership chain, or weak source-of-funds evidence.

[aa btn]Book a Call[/aa]

[/aa]

Why a Panama Company Can't Easily Get GBP and EUR Locally

A Panama company struggles to get GBP and EUR locally because of correspondent banking de-risking, not because the activity is illegal. Panama has featured on enhanced-monitoring lists kept by the Financial Action Task Force and on the UK's own high-risk third countries guidance, so correspondent banks treat Panama-linked flows as higher risk. When a bank decides the compliance cost outweighs the revenue, it simply declines the relationship.

That decision cascades down to the business. A Panama IBC or SA that wants to receive British pounds from a London client cannot route those payments cleanly through a local account that no UK rail will recognise. In practice, a Panama consultancy invoicing a UK agency in GBP finds its Panamanian bank can only offer a slow SWIFT path that the client's bank may then query.

[aa fast-fact]

Fast Fact: Some European banks refuse to accept incoming funds that originate from a Panama bank account outright, treating the source jurisdiction as a reason to de-risk the entire transaction.

[/aa]

Three problems show up repeatedly for a non-resident company UK account applicant:

Local Panama banks favour onshore activity. Most now prefer companies with staff, premises, and a tax footprint inside Panama, and impose high minimum balances on offshore-facing entities.

SWIFT-only access is not enough. A UK client paying by Faster Payments needs a sort code, and an EU client paying into SEPA needs an IBAN. A correspondent SWIFT chain adds days and fees and still does not give the company local collection details.

De-risking is unpredictable. An account can be approved and then closed months later when the correspondent bank revises its risk appetite.

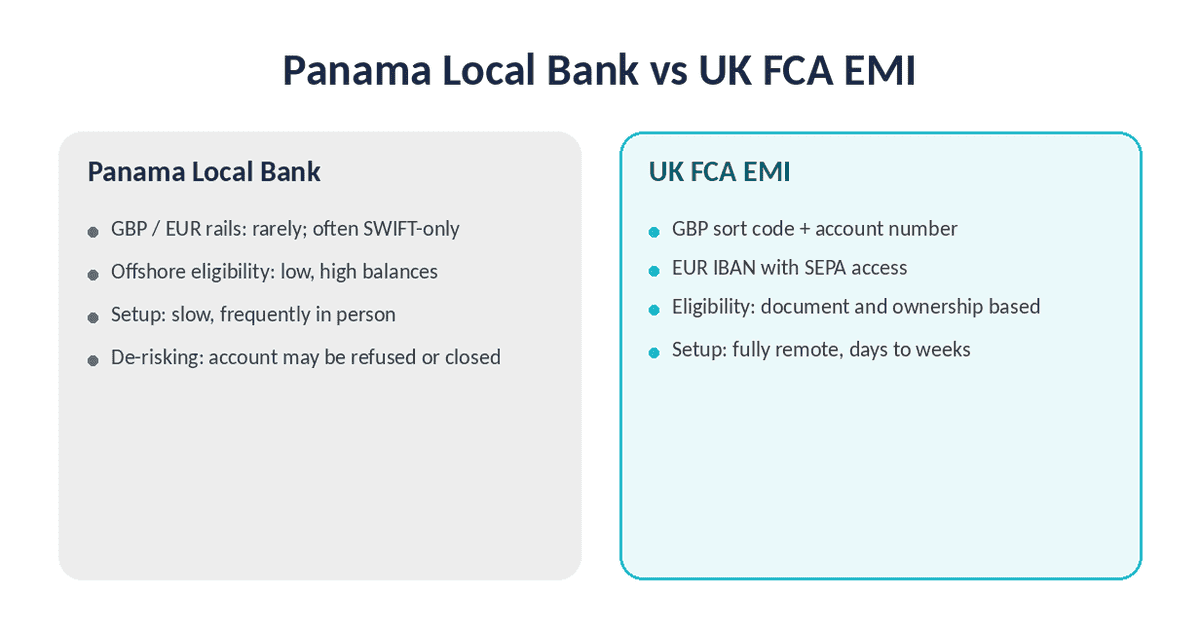

The contrast between the two routes is stark when set side by side:

Route | GBP and EUR local rails | Offshore eligibility | Setup |

|---|---|---|---|

Panama local bank | Rarely; often SWIFT-only | Low; high minimum balances | Slow, frequently in person |

UK FCA EMI | Sort code + EUR IBAN | Document and ownership based | Fully remote |

A UK FCA EMI for offshore company banking sidesteps the correspondent problem by holding GBP and EUR directly on UK and EU payment rails. The friction shifts from "will any bank touch this jurisdiction" to "can the company pass standard verification."

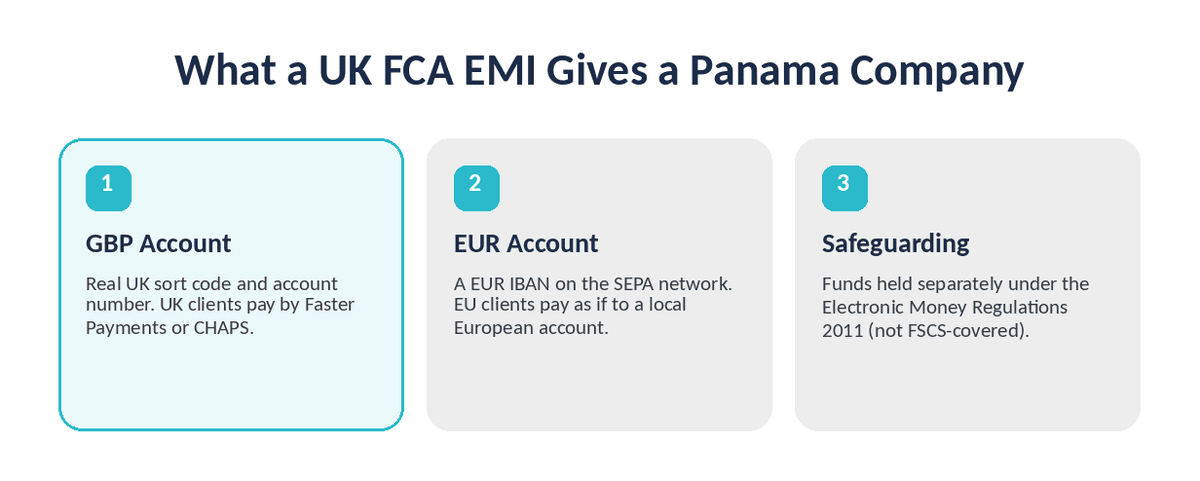

What a UK FCA EMI Gives a Panama Company

A UK FCA-authorised EMI gives a Panama company UK business account GBP EUR functionality: a GBP account with a sort code and account number, and a EUR account with an IBAN, without a Panama bank. The institution holds client money on regulated payment rails and issues local details in the company's name. For a Panama entity locked out of correspondent banking, that distinction decides whether invoices get paid.

An EMI is authorised and supervised by the Financial Conduct Authority, the UK regulator whose register lets anyone verify a firm's authorisation and firm reference number. EQWIRE, for example, operates as a UK EMI under FCA firm reference number 901100.

GBP Sort Code and Account Number

A Panama IBC GBP sort code account works exactly like a UK business account for inbound and outbound sterling. The company receives a six-digit sort code and an eight-digit account number, so UK clients pay by Faster Payments or CHAPS without an international transfer. Faster Payments settles domestic sterling in seconds for most amounts. The practical effect: a London client sees a normal UK account on the invoice, not a foreign SWIFT instruction that their own bank may flag.

EUR IBAN and SEPA Access

The EUR side runs on an IBAN that connects to the Single Euro Payments Area, the scheme governing euro credit transfers across the EU and EEA. An EUR IBAN UK EMI account lets EU customers pay the Panama company as if it held a local European account. Standard SEPA Credit Transfers clear next business day, and SEPA Instant moves up to €100,000 in under ten seconds where supported. The ECB's instant settlement infrastructure underpins much of that speed across the euro area.

How Client Money Is Safeguarded

Here is the part that matters for risk. E-money held in an EMI is safeguarded under the Electronic Money Regulations 2011, which require the institution to hold customer funds separately from its own money, typically in segregated accounts. This is not the same as the Financial Services Compensation Scheme (FSCS), which protects bank deposits up to £85,000. EMI balances are not FSCS-covered. The safeguarding model isolates client funds if the institution fails, but it works differently from deposit insurance, and a Panama company should understand that distinction before moving operating balances. In practice, this suits a trading company that cycles money through the account rather than parking large reserves in it. Verifying the provider's FCA authorisation and reading its safeguarding statement takes minutes and confirms how client money is held.

Before Applying: What a Panama Company Needs Ready

Preparation decides the timeline. A Panama SA business account application that arrives complete clears verification far faster than one that triggers follow-up requests. The institution runs Know Your Business (KYB) checks on the company and Know Your Customer checks on its owners, so both sets of evidence need to be ready before applying.

Corporate Documents

The institution verifies that the company exists and who controls it. A Panama IBC or SA should prepare its Certificate of Incorporation, the Articles of Association, and the register of directors and shareholders. A certificate of good standing helps where the company has existed for more than a year. Documents issued in Spanish often need a certified English translation, and some providers ask for apostilled copies.

Beneficial Ownership and Source of Funds

This is where offshore applications succeed or fail. The applicant must map the ultimate beneficial owners (UBOs) behind any nominee structure and show where the company's money comes from. Expect to provide signed contracts, invoices, or a clear business description that explains the expected flow of GBP and EUR. Nominee directors and opaque ownership are the fastest way to a decline, because the compliance team cannot complete its risk picture.

[aa cta]

Ready to Receive GBP and EUR for Your Panama Company?

Open a multi-currency account with UK and EU rails — a real sort code and EUR IBAN, with no Panama bank required.

[aa btn]Create Account[/aa]

[/aa]

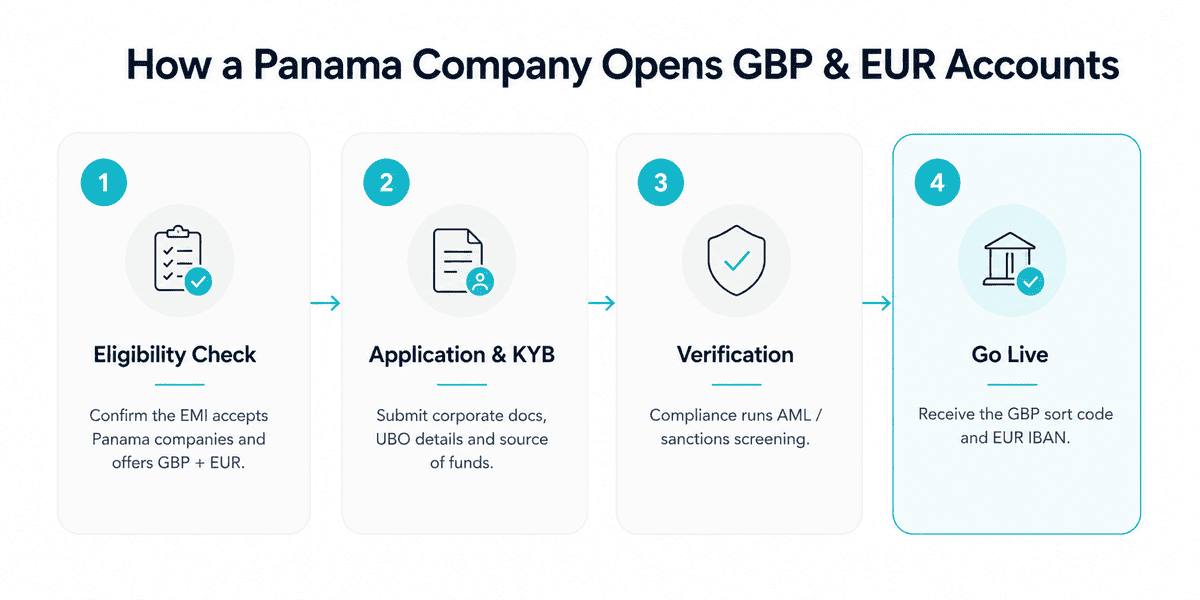

Step-by-Step: Opening GBP and EUR Accounts via a UK FCA EMI

The route runs in four stages: confirm eligibility, submit the application and KYB pack, pass verification, then receive the account details. This is the practical sequence behind the question of how a Panama-registered company opens GBP and EUR accounts via a UK FCA EMI, and most of the work sits in the first two stages.

Step 1: Eligibility Check and Provider Selection

Confirm the provider accepts Panama-incorporated companies before investing time in an application. Acceptance policies differ sharply between EMIs, and some exclude specific jurisdictions or activities. Check the firm's authorisation on the FCA register, read its eligibility policy, and confirm it offers both GBP and EUR local details rather than SWIFT-only access. A comparison of Wise Business against a dedicated FCA EMI shows how provider choice changes the outcome for offshore structures.

Step 2: Application and KYB Submission

Submit the corporate documents, UBO details, and source-of-funds evidence prepared earlier. Describe the business activity in concrete terms: what the company sells, to whom, and in which currencies. A precise description ("software consulting invoiced to UK and German clients in GBP and EUR") clears review faster than a generic line like "international trade."

Step 3: Verification and Account Activation

The compliance team reviews the file, runs sanctions and AML screening, and may request clarification. Responding quickly and completely keeps the application moving. This stage typically takes a few business days to a few weeks, depending on structure complexity and how clean the documentation is.

Step 4: Receiving the Sort Code and EUR IBAN

On approval, the company receives its GBP sort code and account number and its EUR IBAN. At this point a UK sort code for non-resident company use is live: UK clients can pay by Faster Payments, and EU clients can send SEPA transfers into the IBAN. The company can also open a GBP account for a non-UK company structure that mirrors what other offshore entities already use.

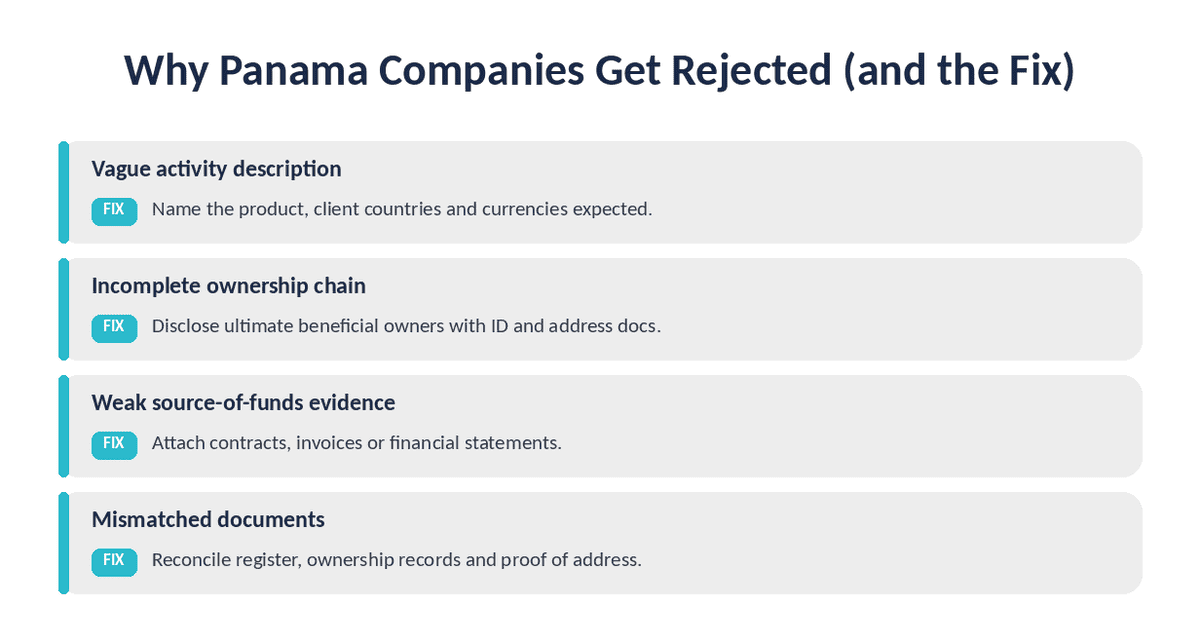

Common Reasons Panama Companies Get Rejected (and How to Fix Them)

Most declines are not about Panama as a country. They are about gaps the compliance team cannot close. A multi-currency account for Panama company applicants is approvable when the file answers every risk question on the first pass.

Vague activity description. "Consulting" or "trading" tells the reviewer nothing. Fix: name the product, the client countries, and the currencies expected.

Incomplete ownership chain. A nominee director with no visible UBO stops the review. Fix: disclose the ultimate owners and supply their identity and address documents.

Weak source-of-funds evidence. A balance with no explained origin reads as risk. Fix: attach contracts, invoices, or financial statements that justify expected volumes.

Mismatched documents. Names or addresses that differ across documents trigger manual review. Fix: reconcile the company register, ownership records, and proof of address before applying.

What this means in practice: a Panama company that prepares a clean ownership map and a specific activity description removes the two factors that cause most offshore rejections.

After Approval: Funding, Receiving, and Converting Between GBP and EUR

Once live, the account operates as day-to-day payment infrastructure. The company receives GBP into its sort code and EUR into its IBAN, holds both currencies, and converts between them when commercially sensible rather than on every receipt. Holding funds in the currency they arrive in avoids paying FX on money that will later go out in the same currency.

Consider a Panama SA that sells digital services to clients in London and Berlin. UK customers pay sterling into its sort code by Faster Payments, EU customers send euro into its IBAN over SEPA, and the company holds both balances. It pays a German subcontractor in euro directly from the EUR balance, with no conversion, and converts to GBP only when it needs to settle a sterling cost. The FX cost falls on the amount actually converted, not on every receipt.

An EMI account has limits worth noting. It is a payment and e-money account, not a lending bank, so it does not offer overdrafts or business credit. EQWIRE, as a regulated UK EMI, also does not facilitate cryptocurrency transactions, and many EMIs apply similar restrictions. The route mirrors how other offshore jurisdictions reach UK and EU rails, so a Panama entity is following a well-worn path rather than an exception.

For a Panama company that trades internationally, the combination of a sort code and an IBAN turns stalled invoices into normal collections. That is the core value of a Panama company UK business account for GBP and EUR: local rails in two of the world's most-used business currencies, opened remotely, without depending on a Panama bank.

FAQ

Step-by-step: how does a Panama-registered company open GBP and EUR accounts via a UK FCA EMI?

A Panama-registered company opens GBP and EUR accounts via a UK FCA EMI in four stages. First, confirm the EMI accepts Panama companies and offers both GBP and EUR local details. Second, submit the corporate documents, beneficial ownership information, and source-of-funds evidence. Third, pass the institution's KYB and AML verification, responding promptly to any clarification request. Fourth, receive the GBP sort code and account number plus the EUR IBAN, after which UK clients can pay by Faster Payments and EU clients by SEPA. The whole process is remote and usually takes from a few business days to a few weeks.

Can a Panama company open a UK business account without a Panama bank?

Yes. A Panama company can open a UK business account for GBP and EUR through a UK FCA-authorised EMI, with no Panama bank account involved. The EMI issues a UK sort code and account number and a EUR IBAN in the company's name, holding the funds on UK and EU payment rails. Eligibility depends on ownership transparency, business activity, and documentation rather than on holding any local Panama banking relationship.

What documents does a Panama IBC need to get a GBP sort code and EUR IBAN?

A Panama IBC GBP sort code and EUR IBAN application generally requires the Certificate of Incorporation, Articles of Association, and the register of directors and shareholders. The institution also asks for identity and address documents for the ultimate beneficial owners, plus source-of-funds evidence such as contracts or invoices. Spanish-language documents may need certified English translations, and some providers request apostilled or notarised copies.

How long does it take to open a GBP and EUR account for a Panama company?

Opening a GBP and EUR account for a Panama company typically takes from a few business days to a few weeks. The timeline depends on how complex the ownership structure is and how complete the documentation is at submission. A clean file with a clear UBO chain and a specific activity description clears verification fastest, while missing or mismatched documents trigger follow-up requests that extend the process.

Why do Panama companies get rejected for a UK business account?

Panama companies usually get rejected for fixable reasons rather than for the jurisdiction alone. The common causes are a vague business activity description, an incomplete ownership chain behind nominee structures, weak source-of-funds evidence, and documents whose names or addresses do not match. Correspondent de-risking makes reviewers cautious about Panama-linked flows, so a transparent ownership map and a precise activity description materially improve the odds of approval.

Panama companies are not shut out of GBP and EUR banking; they are shut out of correspondent banking, and those are different problems. A UK FCA-authorised EMI provides local UK and EU rails directly, so a transparent, well-documented Panama entity can collect sterling and euro without a Panama bank. The decisive factors are eligibility and clean documentation, not the country of incorporation. Preparing a clear ownership map, a specific activity description, and solid source-of-funds evidence removes most of the friction before it starts. For a Panama company that wants a real sort code and a EUR IBAN UK EMI account opened remotely, a regulated provider such as EQWIRE offers a practical, compliant path — start at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)