•

•

Payment Account for Recruitment Agencies: Pay International Contractors in Multiple Currencies

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

A recruitment agency placing contractors across the UK, the EU and the Gulf runs a payment operation that looks nothing like a single monthly payroll. Each cycle means dozens of payouts in GBP, EUR, USD and AED, often on tight placement margins where a few percentage points decide whether a contract is profitable. The global average cost of sending a cross-border payment was 6.49% in Q1 2025, according to World Bank data, and most of that cost is invisible until reconciliation. The right payment account for recruitment agencies removes those layers by holding multiple currencies and paying contractors through local rails instead of one-size-fits-all SWIFT wires. This article compares the three ways agencies actually pay overseas contractors, weighs them on cost, speed and currency coverage, and gives a simple framework for choosing.

[aa key-takeaways]

Key Takeaways

Recruitment agencies generally pay overseas contractors three ways: a high-street business bank, a multi-currency account from an FCA-authorised EMI, or an employer-of-record (EOR) or money-transfer service.

High-street banks cost the most on cross-border payouts because SWIFT routing stacks sender, intermediary and receiver fees on top of a 2–4% FX markup.

A multi-currency account holds GBP, EUR, USD and AED in one place and pays through FPS, SEPA and local rails, so funds avoid the correspondent-bank fee chain.

EOR services solve employment compliance rather than payments; for independent contractors their cost (often $200–800 per worker monthly) is usually unnecessary.

The right choice depends on contractor volume, payment frequency and currency mix rather than brand familiarity.

[aa btn]Book a Call[/aa]

[/aa]

Why Paying International Contractors Is Hard for Recruitment Agencies

Paying international contractors strains agency margins because each cross-border transfer carries costs that a domestic payroll never sees. A single payout can pass through three fee points before it lands, and the exchange rate applied is rarely the rate shown on a currency app. For an agency running many low-margin placements, those deductions compound across every contractor, every cycle.

The cost sits in two places. The first is the fee chain on a traditional SWIFT wire. The second is the foreign-exchange markup banks add when converting the agency's GBP into the contractor's currency.

[aa fast-fact]

Fast Fact: The global average cost of sending a cross-border payment was 6.49% in Q1 2025 (World Bank). On a £4,000 contractor payout, that is roughly £260 lost to fees and FX before the contractor sees a penny.

[/aa]

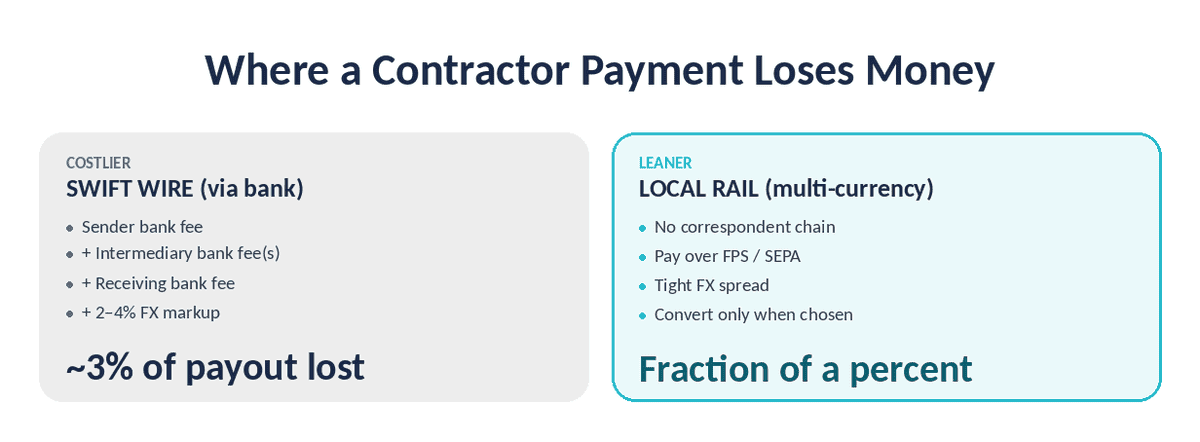

Here is where the money is lost. A SWIFT payment routed through the correspondent banking network can be handled by one or more intermediary banks, and each may deduct a handling fee before passing the funds on. The agency pays a sending fee, the contractor often receives less than the invoice amount, and neither party controls the deductions in between. Bank FX markups commonly run 2–4% above the mid-market rate, a cost buried in the exchange rate rather than shown as a line item.

For a staffing business, the practical consequence is unpredictable net pay for contractors and eroded margin for the agency. Cross-border contractor payments also settle slowly through this route, typically taking one to five business days, which complicates cash flow when a client pays late but contractors expect funds on a fixed date.

Consider an agency placing thirty contractors each month across Germany, the United States and the UAE. If every €3,000 to £4,000 payout loses around 3% to fees and exchange-rate markup, the agency hands over several thousand pounds a cycle on payment friction alone. Across a year, that adds up to the cost of a full-time hire, spent on the plumbing between the agency's account and its contractors rather than on growth. The contractors feel it too, because the amount that lands rarely matches the invoice, which prompts queries the finance team then has to reconcile by hand.

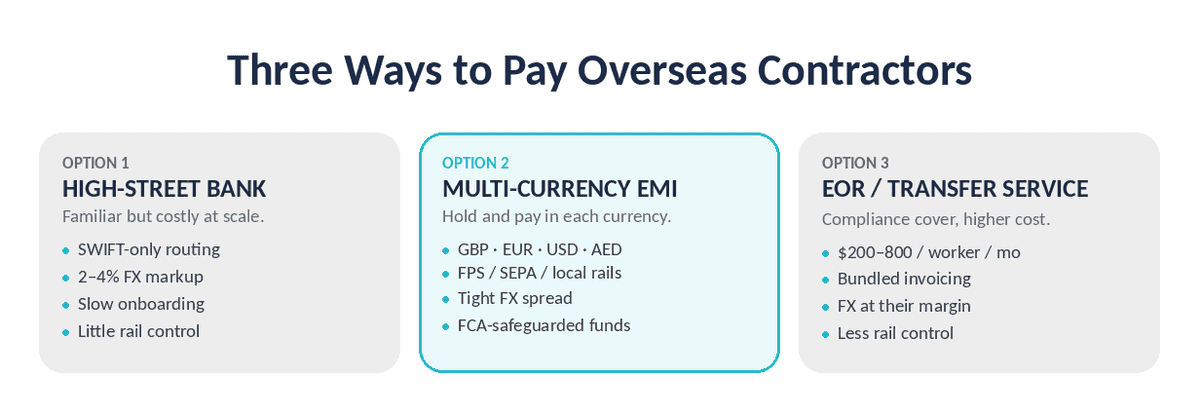

The Three Ways Recruitment Agencies Pay Overseas Contractors

Recruitment agencies generally pay overseas contractors in one of three ways. Each suits a different stage of growth, contractor mix and appetite for compliance overhead.

High-Street Business Bank Account

A high-street business bank account is the default starting point, and the most expensive at scale. Onboarding can take weeks, international payments route almost exclusively through SWIFT, and currency conversion happens automatically at the bank's marked-up rate. Most UK business banking packages were built for domestic trade, so paying a contractor in Dubai or Berlin is treated as an exception rather than a core function.

Control is the other limitation. Agencies rarely choose the rail, cannot hold the contractor's currency, and see FX applied on every receipt and payout. Many banks also cap or scrutinise high volumes of outbound international payments, which can stall a payroll run during periods of growth. For an agency adding contractors faster than its bank can process them, that friction becomes an operational risk rather than a minor cost.

Multi-Currency Payment Account (FCA-Authorised EMI)

A multi-currency account from an FCA-authorised electronic money institution (EMI) holds several currencies in one place and pays through local rails wherever possible. The agency can keep GBP, EUR, USD and AED as separate balances, receive client funds in the currency of invoice, and pay each contractor without forcing a conversion on every transaction.

This is the same multi-currency setup that import-export businesses use to manage several currencies side by side. For an agency, it turns a scattered set of wires into a single account that pays UK contractors over Faster Payments, EU contractors over SEPA, and Gulf contractors through supported currency corridors.

EOR and Contractor-Payment Platforms

An employer of record (EOR) becomes the legal employer of a worker abroad and handles local payroll, tax and benefits. That model solves employment compliance, but independent contractors are not employees, so the overhead is often unnecessary for pure payouts. EOR pricing typically runs $200–800 per worker per month or 10–15% of salary, while lighter contractor-payment platforms charge roughly $25–49 per contractor per month and bundle invoicing with FX at their own margin.

These services add convenience and, for EORs, genuine legal cover. The trade-off is cost per head and less direct control over the exchange rate and the underlying payment rail.

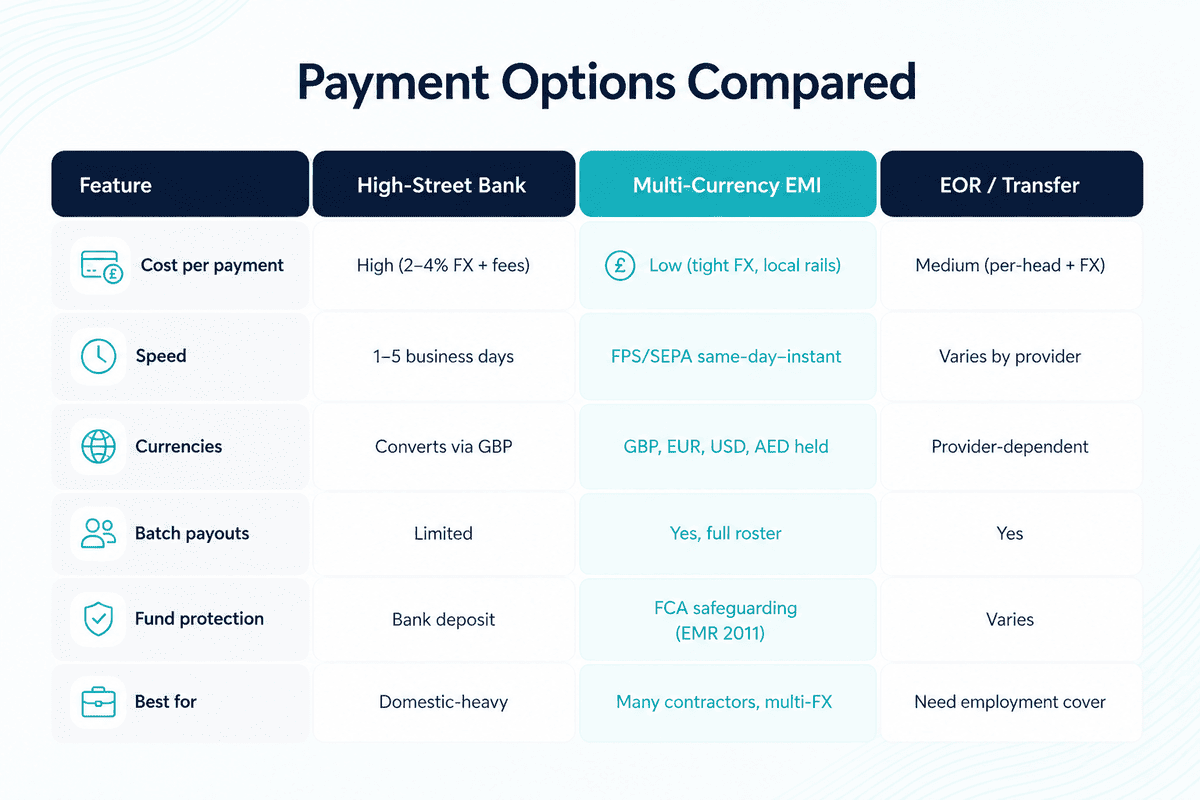

Comparing the Options on Cost, Speed and Currency Coverage

The clearest way to choose is to compare the three routes on the metrics that actually move agency margin: the true cost per payment, settlement speed, and how many currencies the account can hold and reach.

[Visuals - Payment Option Comparison Table - Table comparing bank, multi-currency EMI account and EOR/transfer service across cost, speed, currency coverage, control and fund protection]

True Cost Per Payment (Fees + FX Spread)

The true cost of a contractor payment is the transfer fee plus the FX spread, and the spread is where most of the difference lives. A high-street bank often applies a 2–4% markup over the mid-market rate and adds SWIFT handling fees on top. A multi-currency account from an EMI typically narrows the FX spread to a fraction of that and avoids intermediary fees by paying on local rails. Across a roster of contractors, a one to three percentage-point difference per payment is the gap between a profitable desk and a marginal one.

A worked example makes the gap concrete. On a £4,000 payout to a contractor in the EU, a 3% bank markup costs roughly £120 in hidden FX, plus a wire fee of perhaps £20 to £30. The same payout through a multi-currency account holding euros, released over SEPA, might cost a fraction of a percent in FX and little or nothing on the transfer itself. Repeated across thirty contractors, the bank route can cost an agency over £4,000 a month that a multi-currency setup keeps. The saving is not a one-off; it recurs on every cycle, which is why finance teams treat the per-payment spread as a structural cost rather than a line item.

Settlement Speed and Currency Reach (GBP, EUR, USD, AED)

Speed depends on the rail, not the provider's marketing. A GBP payout to a UK-based contractor over Faster Payments usually arrives within minutes. A euro payment over SEPA Instant settles in around ten seconds end-to-end, where supported, against the one-to-five-day window typical of a SWIFT wire. Currency reach matters just as much: an agency paying contractors in Dubai needs an account that can hold and send AED, the same way a digital-nomad account holds GBP, EUR, USD and AED together rather than converting everything back to sterling.

[aa cta]

Pay Every Contractor in Their Currency, From One Account

Hold GBP, EUR, USD and AED, receive client funds in the currency of invoice, and pay contractors on local rails instead of costly SWIFT wires.

[aa btn]Open a Business Account[/aa]

[/aa]

Compliance, Fund Protection and Control

Cost and speed mean little if funds are not protected. An FCA-authorised EMI does not hold a banking licence, so e-money balances are not covered by the Financial Services Compensation Scheme. Client money is instead safeguarded in segregated accounts under the Electronic Money Regulations 2011, kept separate from the institution's own funds. UK payment firms also operate under the FCA's Consumer Duty, which sets expectations on fair pricing and clear communication. The practical point for an agency: an EMI account offers strong fund protection and direct control over rails and currencies, while an EOR offers employment-law cover the agency may not need for contractors.

When Does a Multi-Currency Payment Account Make Sense for Your Agency?

A multi-currency account earns its place once an agency pays more than a handful of overseas contractors or works across several currencies. Below that threshold, a basic bank account may be tolerable. Above it, the FX and fee savings start to compound quickly.

By Contractor Volume and Payment Frequency

Volume is the first trigger. An agency paying five contractors once a month feels the cost less than one running weekly payouts to thirty. Batch payments matter here: a multi-currency account that supports bulk contractor payments lets the finance team upload one payment file and release a full roster in a single run, rather than keying wires one by one. This also reduces the operational risk of a mistyped IBAN holding up a payroll cycle.

By Currency Mix and Corridor

Currency mix is the second trigger. An agency that only ever pays UK contractors in GBP has little need for multiple balances. One placing contractors in Berlin, New York and Dubai needs to hold EUR, USD and AED and reach each on the most efficient corridor. The wider the currency spread, the more a single multi-currency account beats a bank that converts everything through sterling.

There is also a timing benefit that finance teams value once they see it. Holding the contractor's currency in advance lets an agency lock in a rate when it suits the business, instead of accepting whatever rate the bank applies on the day a payment goes out. An agency that receives a client invoice in euros can keep those euros and pay euro-based contractors from the same balance, so the funds never convert to sterling and back. That removes a round-trip of FX cost on money that was always destined for the eurozone, and it shields the agency from currency swings between invoicing a client and paying the contractor weeks later.

How a UK recruitment agency pays overseas contractors in GBP, EUR, USD and AED without SWIFT fees comes down to this combination: hold the contractor's currency in advance, then release it on a local rail so the payment never enters the correspondent-bank chain.

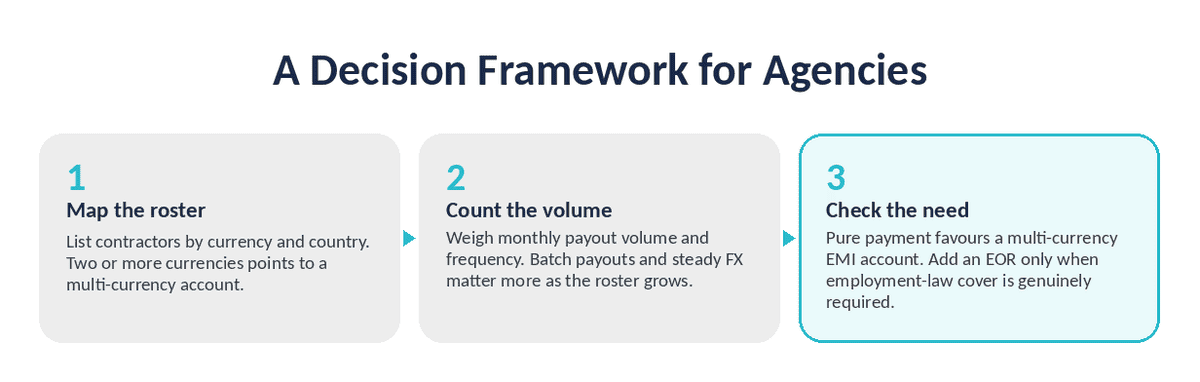

A Decision Framework for Recruitment Agencies

Choosing a setup is less about the provider's brand and more about matching the account to how the agency actually pays. A short framework helps decision-makers weigh the trade-offs.

First, map the contractor roster by currency and country. If most payouts sit in two or more currencies, a multi-currency account vs business bank account comparison almost always favours the multi-currency option on cost. Second, count the monthly payment volume; batch payouts and predictable FX become more valuable as the roster grows. Third, decide whether the agency needs employment-law cover or only needs to pay independent contractors. Where the answer is pure payment, an EOR's per-head cost is hard to justify, and a payment account for recruitment agencies built on an FCA-authorised EMI usually delivers the lowest total cost with the most control.

The agencies that get this right treat payments as infrastructure, not an afterthought. Holding the right currencies, routing through local rails, and keeping client funds safeguarded turns contractor payouts from a margin leak into a predictable, low-cost process. EQWIRE's currency network covers 66 currencies with T+0 to T+2 settlement windows, including AED, so agencies can pay contractors across the UK, EU and Gulf from one account. For agencies still weighing a platform against a familiar bank, a closer look at how an FCA EMI compares to a mainstream payment platform is a sensible next step.

FAQ

How does a UK recruitment agency pay overseas contractors in GBP, EUR, USD and AED without SWIFT fees?

A UK recruitment agency avoids SWIFT fees by holding each currency in a multi-currency account and paying contractors through local rails rather than international wires. GBP payouts to UK-based contractors go over Faster Payments, EUR payouts over SEPA, and other currencies such as AED route through supported local corridors. Because the funds are already held in the contractor's currency, the payment does not pass through the correspondent-banking chain that adds intermediary fees and FX markup. The agency converts currency only when it chooses to, at a tighter spread, instead of on every transfer.

Multi-currency account vs business bank account: which is cheaper for contractor payments?

For agencies paying contractors in more than one currency, a multi-currency account is usually cheaper than a traditional business bank account. High-street banks typically apply a 2–4% FX markup and route payments through SWIFT, which adds layered handling fees. A multi-currency account from an FCA-authorised EMI narrows the FX spread and uses local rails, so the cost per cross-border contractor payment drops. The saving grows with payment volume and the number of currencies involved.

How to pay contractors in different currencies from one account?

To pay contractors in different currencies from one account, an agency uses a multi-currency account that holds separate balances for each currency, such as GBP, EUR, USD and AED. Client payments are received in the currency of invoice and held without forced conversion, then released to each contractor on the local rail for that currency. Many providers support batch or bulk payments, so a finance team can pay an entire contractor roster in a single upload rather than processing wires individually.

Do recruitment agencies need an employer of record to pay contractors?

Recruitment agencies usually do not need an employer of record (EOR) to pay independent contractors. An EOR becomes the legal employer and handles local payroll, tax and benefits, which suits hiring full employees abroad rather than paying contractors. For contractor payouts, an EOR's cost, often $200–800 per worker per month or 10–15% of salary, adds expense without a matching benefit. A multi-currency payment account covers the payment need directly, while agencies that require local employment compliance can consider an EOR alongside it.

Is a multi-currency account safe if the provider is an EMI rather than a bank?

A multi-currency account from an FCA-authorised electronic money institution (EMI) protects client funds through safeguarding rather than deposit insurance. E-money balances are not covered by the Financial Services Compensation Scheme, but under the Electronic Money Regulations 2011 the institution must hold client money in segregated accounts, separate from its own funds. This means agency and contractor funds are ring-fenced if the provider fails. EMIs are authorised and supervised by the FCA and operate under the Consumer Duty, giving agencies a regulated, transparent alternative to a high-street bank.

For a recruitment agency, the cost of paying international contractors is a choice of infrastructure rather than a fixed overhead. A high-street bank keeps things familiar but quietly erodes margin on every cross-border payout. A multi-currency account holds GBP, EUR, USD and AED, pays on local rails, and keeps funds safeguarded under FCA rules, while an EOR earns its place only when the real need is employment compliance rather than payment. Agencies that match the account to their contractor volume and currency mix protect both their margin and their contractors' trust. A payment account for recruitment agencies built for cross-border payouts pays for itself across a single busy cycle, and agencies can open one at https://client.eqwire.com/sign-up.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)