•

•

REST API for Multi-Currency Payouts: How Marketplaces Can Pay Sellers in GBP, EUR and USD

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

[Visuals - REST API Multi-Currency Payouts Cover - Cover image showing a marketplace paying sellers in GBP, EUR and USD through a single REST API]

A marketplace that pays 500 sellers every Friday carries a quiet operational tax: exporting bank files and reconciling which payments actually landed, with every currency converted by hand. At scale, that process breaks. A REST API for multi-currency payouts replaces it with one repeatable call sequence that pays sellers in GBP, EUR and USD without manual conversion.

This guide reads as an integration playbook for engineering and finance-operations teams. It covers what to put in place before building, the four-step call sequence that moves money to a seller, how to handle idempotency and failed payments, and a pre-launch checklist for going live. The emphasis is implementation detail. The gap between a payout system that survives peak volume and one that double-pays sellers comes down to a few decisions made during integration.

[aa key-takeaways]

Key Takeaways

A REST API for multi-currency payouts replaces manual bank files with one repeatable call sequence.

The core flow is four calls: create payee, request an FX quote, submit the payout, then confirm settlement via webhook.

Bulk endpoints pay hundreds of sellers in GBP, EUR and USD in a single request.

An idempotency key on every request stops a network retry from paying a seller twice.

A sandbox run should sign off the integration before any live money moves.

A UK FCA-authorised Electronic Money Institution (EMI) safeguards seller funds in segregated accounts.

[aa btn]Book a Call[/aa]

[/aa]

Before Integrating a REST API for Multi-Currency Payouts

A marketplace payout API is a programmatic connection that lets a platform instruct payments to many recipients, across currencies and payment rails, without anyone touching a bank portal. It standardises a messy manual task into structured requests and responses.

Most platforms reach for one only after the alternatives stop working. Manual transfers and exported bank files are fine for a handful of payments, but they scale badly: every currency is converted by hand, and reconciliation becomes a weekly chore. Built-in payouts from a payment service provider help, yet they often limit which currencies a platform can pay and apply an FX rate the platform does not control. A dedicated payout API gives back control over currency, rail, and timing, which is why marketplaces with growing seller bases tend to migrate toward one.

Two foundations sit underneath that connection. The first is a place to hold money. The second is a clean record of who gets paid. Both need to exist before the first payout call goes out.

Multi-Currency Account and API Credentials

The account is the funding source. To pay sellers in three currencies without converting on every transaction, a marketplace holds balances in each one. A single multi-currency account that holds GBP, EUR and USD lets the platform fund a euro payout from euros it already holds, rather than buying euros at the moment of payment.

Credentials come next. Most providers issue two sets of API keys: one for a sandbox, one for production. The sandbox mirrors live behaviour without moving real funds, which makes it the safe place to build and test.

In practice: a platform that already receives PSP settlements from Adyen, Stripe or PayPal into a multi-currency account can fund seller payouts from the same balances, closing the loop between collection and payout inside one ledger.

Mapping Sellers to Verified Payees

A payout needs a destination. In API terms, that destination is a payee (sometimes called a beneficiary): a stored record holding a seller's name, bank details, country, and currency. Creating the payee once means later payouts reference an ID instead of resending full bank data.

Payee records also carry the compliance weight. A regulated provider runs know-your-customer (KYC) checks on payees before money can reach them. Mapping each marketplace seller to a verified payee turns onboarding friction into a one-time step rather than a per-payment delay.

[aa fast-fact]

Fast Fact: SEPA Credit Transfers typically settle same-day or by the next business day, while SEPA Instant moves funds in under 10 seconds for amounts up to €100,000 per transaction.

[/aa]

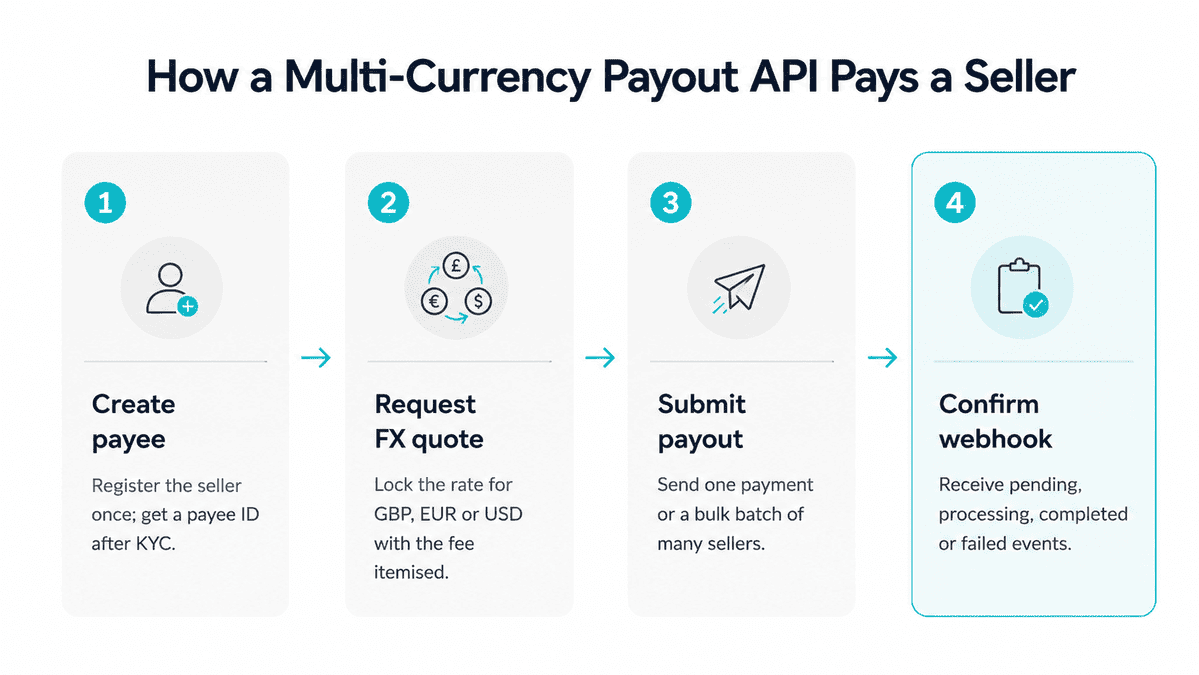

Step-by-Step: Paying Sellers via the API

Paying sellers through a multi-currency payout API follows four calls in sequence:

Create and verify the payee.

Request an FX quote for the target currency.

Submit the payout, as a single payment or in bulk.

Confirm settlement through a webhook.

Each step maps to one API call and one clear response. The sections below walk through what happens at each stage and where teams tend to trip.

Step 1: Create and Verify the Payee

The first call registers the seller as a payee and returns a payee ID. That ID becomes the stable reference for every future payment to that seller. Verification status travels with the record, so the integration can check that a payee has cleared KYC before attempting to pay them.

A clean payee model prevents a common failure: paying the right amount to stale or unverified bank details.

Step 2: Request an FX Quote for GBP, EUR or USD

The second call asks the API what the conversion will cost. When the funding balance and the payout currency differ, the provider returns a quote that locks the exchange rate and itemises the fee for a short window, often 30 to 60 seconds.

That quote-and-lock model is what removes manual FX conversion from the process. The marketplace sees the exact settled amount before committing, so the figure that appears in the quote is the figure that leaves the account. Paying a euro balance into a euro payout skips conversion entirely, which is why holding the right currencies matters.

This is also where margin quietly leaks. When a provider bundles the fee into the exchange rate rather than itemising it, the true cost of each payout is hard to see and harder to forecast. An itemised quote separates the FX spread from the transfer fee, so a finance team can model payout costs per currency and decide when to convert in bulk rather than per payment. Holding GBP, EUR and USD and settling like-for-like keeps conversion to the moments a platform actually chooses it.

Step 3: Submit the Payout (Single and Bulk)

The third call moves the money. For a single seller, the request references the payee ID, the amount, the currency, and the locked quote. The response returns a payout ID and an initial status of pending.

Volume changes the shape of the call. A bulk payout API for sellers accepts an array of payouts in one request, so a marketplace can pay hundreds of recipients in GBP, EUR and USD without firing hundreds of separate calls. Each item in the batch keeps its own payout ID and status, which keeps reporting clean even when one payment in a run fails.

In practice, a marketplace running a weekly settlement cycle for 500 UK and EU sellers submits one batch on payout day. GBP recipients route over Faster Payments, EUR recipients over SEPA, and the platform receives a status event per seller rather than chasing 500 confirmations. A single failed item surfaces on its own, so the operations team investigates one payment instead of auditing the whole run.

Step 4: Confirm Settlement via Webhook

The fourth step is where reconciliation happens. Rather than polling the API every few seconds, the integration registers a webhook and lets the provider push status changes as they occur. A payout moves through pending, processing, completed, or failed, and each transition fires an event.

Webhook-driven status is the reliable way to know money actually arrived. EQWIRE's guide to webhook integration for payment reconciliation shows how those events update a ledger automatically, so finance teams see a settled payout without manual checking.

Rail selection sits underneath all four steps. A GBP payout can route over Faster Payments for near-instant delivery, a EUR payout over a SEPA Credit Transfer governed by the European Payments Council, and a USD payout over SWIFT, which typically settles in one to five business days depending on the correspondent chain. The Bank of England oversees the UK payment systems that carry domestic transfers, including CHAPS for high-value GBP payments.

[aa cta]

Stop Building Payout Plumbing From Scratch

Open a multi-currency EQWIRE account and pay sellers in GBP, EUR and USD through one API, with FX, rails, and reconciliation handled.

[aa btn]Create Account[/aa]

[/aa]

Handling Errors and Edge Cases

A payout integration earns its keep in the failure paths. Networks drop requests, banks reject details, and currencies occasionally mismatch. Designing for these cases up front prevents the two outcomes that hurt most: paying a seller twice, or believing a failed payment succeeded.

Idempotency and Retries

An idempotency key is a unique identifier attached to a payout request so a retry never creates a duplicate payment. When the client sends the same key twice, the API recognises the repeat and returns the original result instead of moving money again.

This matters because retries are normal. A timeout often means the request succeeded but the response was lost, and a blind retry without an idempotency key would pay the seller a second time. With the key in place, the seller is paid once and the ledger stays clean.

The cost of getting this wrong is rarely a single mistake. At high volume, a retry storm during an outage can duplicate dozens of payments before anyone notices, and clawing back money already sent to sellers is slow and damages trust. Treating the idempotency key as mandatory on every request, including bulk batches, turns that risk into a non-event.

Failed Payouts, Returns and Currency Mismatches

Not every payout completes, and the integration needs a defined response to each failure type. A payment can fail at submission, settle and then bounce back as a return, or stall because the payee currency does not match the destination account.

The webhook stream is what surfaces these states. A failed event should trigger a review rather than an automatic resend, since the cause is often bad payee data that a retry will not fix. Returns need the funds credited back to the source balance and the payee flagged for correction. Handling each path explicitly keeps a high-volume payout run auditable, which is exactly how marketplaces pay sellers across currencies without losing track of edge cases.

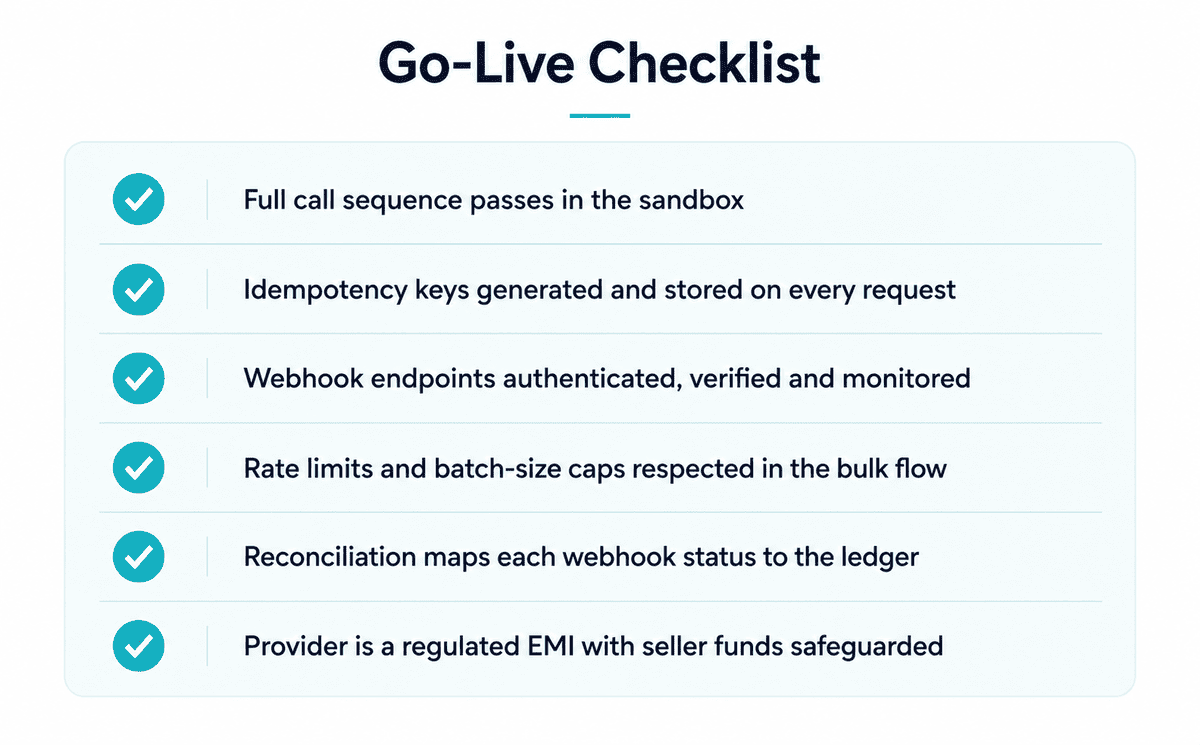

Going Live: A Pre-Launch Checklist

Before the first live payout, a short checklist separates a controlled launch from an incident. Most items take an afternoon and prevent problems that are expensive to fix once real money is in flight.

A pre-launch review should confirm the following:

The full call sequence passes in the sandbox, including a deliberately failed payout and a duplicate-key retry.

Idempotency keys are generated and stored for every request.

Webhook endpoints are authenticated, verified, and monitored for missed events.

Rate limits and batch-size caps are understood and respected in the bulk flow.

Reconciliation maps each webhook status back to the internal ledger.

The provider is a regulated institution, with seller funds safeguarded.

That final point is a due-diligence step, not a formality. Where a marketplace holds and pays out seller money, the regulatory status of the provider decides how that money is protected. A UK Electronic Money Institution authorised by the FCA must keep client funds in segregated accounts under the Electronic Money Regulations 2011. A platform can verify a provider's authorisation directly on the FCA Financial Services Register. For teams weighing providers, the trade-offs between an unregulated tool and a regulated EMI are covered in EQWIRE's comparison of Wise Business and a UK FCA EMI.

Monitoring deserves a line of its own. A payout system that runs unattended needs alerting on missed webhooks, on payouts stuck in processing past an expected window, and on any spike in failed events. These signals catch a broken integration before sellers start asking where their money is, and they give the operations team a clear first place to look.

UK EMI payouts carry a known constraint worth stating plainly. SEPA reaches the EU and EEA only, and SWIFT fees vary by the correspondent chain a payment travels through, so currency reach and cost depend on the rails a provider supports. A platform serving sellers outside SEPA coverage should confirm its provider can route those payments before committing to a launch date.

FAQ

How do online marketplaces use REST APIs to pay sellers in GBP, EUR and USD without manual FX conversion?

Online marketplaces use REST APIs to pay sellers in GBP, EUR and USD without manual FX conversion by funding each payout from a matching currency balance and using a quote-and-lock step when conversion is needed. The platform holds GBP, EUR and USD in a multi-currency account, so a euro payout draws from euros already held. When the funding and payout currencies differ, the API returns a locked FX quote with the fee itemised before the payout is confirmed. The marketplace never converts money by hand or guesses the rate, because the quoted settled amount is the amount that leaves the account.

How do you send a bulk payout to many sellers at once?

A bulk payout API for sellers accepts an array of individual payouts inside a single request, each with its own payee ID, amount, and currency. The provider processes them as a batch while keeping a separate status and payout ID for every item, so one failed payment does not stop the rest. This lets a marketplace pay hundreds of sellers across GBP, EUR and USD in one call rather than looping through individual requests, which keeps both performance and reporting manageable at scale.

What is an idempotency key and why does it matter for payouts?

An idempotency key is a unique value attached to a payout request that lets the API detect and ignore duplicates. If a network error causes the client to resend the same request, the API matches the key and returns the original outcome instead of issuing a second payment. For payouts, this is the safeguard that prevents paying a seller twice when a response is lost, and it keeps the ledger accurate during the retries that occur in any production system.

How do you test multi-currency payouts before going live?

Testing happens in a sandbox environment that mirrors production without moving real funds. The integration should run the complete sequence there: creating a payee, requesting an FX quote, submitting both single and bulk payouts, and receiving webhook events for each status. A thorough test also forces the failure paths, including a rejected payout and a duplicate-key retry, to confirm the system handles them correctly before any live money is involved.

Do marketplaces need a separate account for each currency?

No. A single multi-currency account can hold GBP, EUR and USD balances at the same time, which removes the need to open and manage a separate banking relationship for each currency. Holding balances in the currencies sellers are paid in also reduces conversion, since like-for-like payments skip FX entirely. Conversion applies only when a marketplace chooses to convert, not on every payout.

A REST API for multi-currency payouts turns a manual, error-prone task into infrastructure a marketplace can rely on at scale. The four-step flow of payee, quote, payout, and webhook stays the same whether a platform pays five sellers or five thousand, and the engineering details around idempotency and failure handling are what keep it dependable. Choosing a regulated provider adds the protection that matters when a platform holds other people's money. EQWIRE offers FCA-authorised multi-currency accounts built to pay sellers in GBP, EUR and USD through one integration, with safeguarding, FX, and local rails handled. Teams ready to move from manual files to an API can open an account and start in a sandbox.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)