•

•

East Caribbean Dollar (XCD) Payments: How to Send and Receive XCD from the UK

[aa disclaimer]

Legal Disclaimer: This article is for informational purposes only and does not constitute legal, financial, compliance, or tax advice. Banking eligibility, regulatory requirements, and provider policies vary by jurisdiction. Consult qualified professionals before making decisions.

[/aa]

UK businesses trading with the Eastern Caribbean run into the same surprise every time: the East Caribbean dollar does not move like the euro or the US dollar. There is no SEPA equivalent and no instant rail, so XCD East Caribbean dollar payments between the UK and the region travel over SWIFT, usually through a US dollar correspondent bank before they ever reach a Caribbean account. The currency is issued by the Eastern Caribbean Central Bank and pegged to the US dollar at a fixed 2.70, which keeps its value steady but adds an extra conversion step on the way in or out. This guide explains how UK companies send and receive XCD, what the route actually costs, how long it takes, and how to cut the hidden deductions that erode each transfer.

[aa key-takeaways]

Key Takeaways

The East Caribbean dollar (XCD) is the shared currency of eight Eastern Caribbean states and is pegged to the US dollar at a fixed rate of 2.70.

No UK bank sends XCD directly. Every payment runs over SWIFT and is settled through a US dollar correspondent bank before conversion to XCD locally.

Each correspondent or intermediary bank in the chain can deduct roughly $10–50, so the amount that arrives is often less than the amount sent.

Most UK businesses pay in GBP and the funds convert GBP→USD→XCD, creating two FX legs even though the USD-to-XCD leg is fixed by the peg.

Correspondent SWIFT transfers to the region typically settle in two to five business days.

Holding US dollars in a multi-currency account removes one FX leg and makes arrival amounts far more predictable.

[aa btn]Book a Call[/aa]

[/aa]

What Is the East Caribbean Dollar (XCD)?

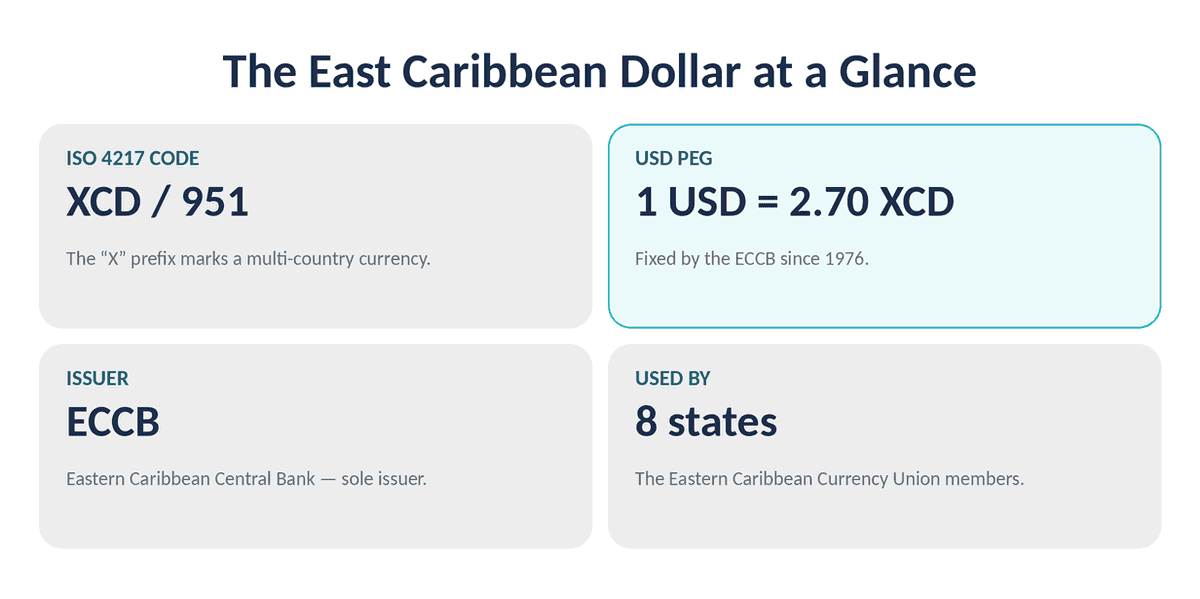

The East Caribbean dollar (XCD) is the shared currency of eight Eastern Caribbean states, issued by the Eastern Caribbean Central Bank and pegged to the US dollar at 2.70. Its ISO 4217 code is XCD, with numeric code 951, listed on the official ISO currency code register. The "X" prefix is a useful tell: it marks a currency issued by a multi-country monetary authority rather than a single national government, which is exactly why XCD payments behave differently from a normal one-country currency.

That shared structure matters for anyone sending money to the Eastern Caribbean. A single central bank controls issuance and holds the region's foreign reserves, so the currency stays stable across all member states.

The USD Peg and Why It Matters for Payments

The peg fixes one US dollar at 2.70 East Caribbean dollars, a rate the ECCB has held since 1976. Nearly fifty years of stability makes XCD predictable for pricing contracts and invoices.

For payments, the peg has a practical consequence. Because XCD is anchored to the dollar, the entire international banking system treats US dollars as the natural gateway into the currency. A UK business almost never moves pounds straight into XCD. The money becomes US dollars first, then converts to East Caribbean dollars at the destination, where the fixed rate applies.

Which Countries Use XCD

Eight members of the Eastern Caribbean Currency Union use the East Caribbean dollar: Antigua and Barbuda, Dominica, Grenada, Saint Kitts and Nevis, Saint Lucia, Saint Vincent and the Grenadines, Anguilla, and Montserrat.

The currency is freely convertible, and jurisdictions such as Saint Lucia operate with no exchange controls. A UK company can therefore pay or be paid in XCD without capital restrictions, though the routing and cost still demand attention.

How XCD Payments Move Between the UK and the Caribbean

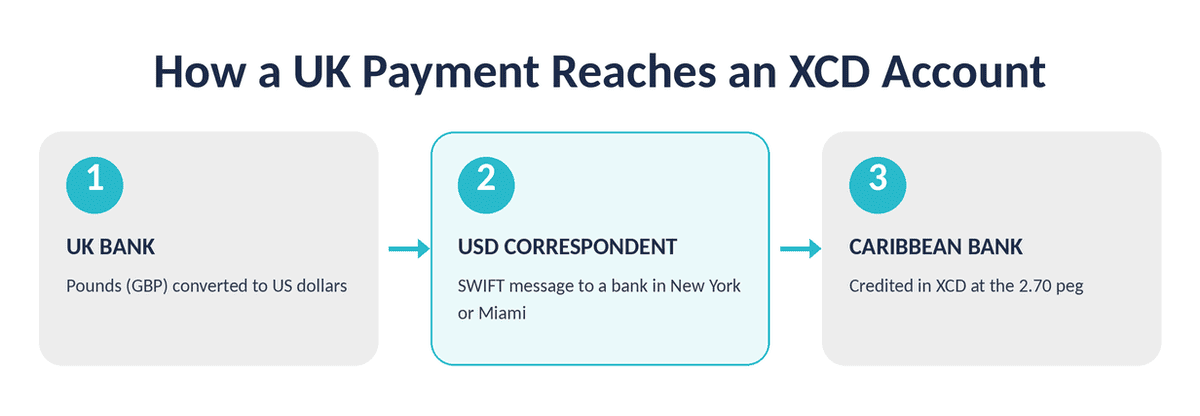

No UK bank sends XCD directly. Payments route over SWIFT through a US dollar correspondent bank, and the funds convert to East Caribbean dollars at the beneficiary's Caribbean bank. SWIFT itself only carries the payment instruction between banks; as explainers of the SWIFT network note, it does not hold funds or settle the transaction, so the actual movement of money depends on the chain of banks involved.

That chain is where East Caribbean dollar transfers gain their cost and their delay. Understanding the two structural reasons behind it helps a finance team set the right expectations.

Why There Is No SEPA Route for XCD

SEPA covers euro payments inside Europe, so it cannot carry XCD, and the UK's Faster Payments system only moves domestic sterling. Neither rail reaches the Eastern Caribbean. Every XCD payment from the UK therefore falls back on SWIFT, the global messaging network that connects banks across borders.

This is the first thing that catches businesses out. A company used to near-instant SEPA transfers for European suppliers finds that the Caribbean equivalent is slower, costlier, and far less transparent.

The Role of USD Correspondent Banks

A correspondent bank is an intermediary that holds accounts for other banks and passes payments along on their behalf, which lets a UK bank reach a Caribbean bank it has no direct relationship with. As Wise describes the intermediary step, the payment can pass through one or more of these banks before arriving.

For the Eastern Caribbean, that intermediary is almost always a large US dollar clearing bank in New York or Miami. A typical journey looks like this: the UK bank converts pounds to dollars, sends the dollars over SWIFT to a US correspondent, and the correspondent forwards them to the beneficiary's bank in the region, which credits the account in XCD at the 2.70 peg. Each hop adds time, a fee, and another point where the payment can stall for compliance checks.

How to Send XCD from the UK (Step by Step)

The most important step comes before any money moves: confirm with the recipient whether their account is credited in XCD or in US dollars, because it changes the details required. Once that is clear, sending follows a predictable order.

Collect the beneficiary details. Account holder name, account number, the bank's SWIFT/BIC code, the bank name and address, and the destination currency (XCD or USD).

Confirm the intermediary bank. Many Caribbean banks publish a required US dollar correspondent for incoming payments. Sending without it is the most common cause of delayed or returned transfers.

Choose the charge code. OUR means the sender pays all fees and the recipient gets the full amount; SHA splits them; BEN takes fees from the transfer itself. For supplier payments, OUR protects the relationship by guaranteeing the invoiced sum arrives.

Initiate the SWIFT payment. A UK business can send through its bank or through a provider that offers a SWIFT business account, then track the payment by its reference.

Keep the confirmation. The SWIFT reference lets either side trace the payment if it stalls at a correspondent.

This is also where the choice to send/receive XCD from a UK business account over SWIFT through a provider, rather than a high-street bank, starts to pay off. Specialist accounts surface the correspondent route and the charge code clearly, which removes most of the guesswork. EQWIRE's guide to running supplier payments without relying on raw SWIFT wires shows how routine payouts can be structured to avoid per-wire correspondent deductions.

How to Receive XCD Payments from the UK

Receiving works in reverse, and the same correspondent logic applies. A UK business expecting funds from an Eastern Caribbean client will usually receive US dollars rather than XCD, because the dollar is the currency that crosses the border. The recipient's bank then converts to pounds if the account cannot hold USD.

To receive cleanly, a UK company should share its account name, sort code or IBAN, its bank's SWIFT/BIC, and ideally a US dollar account if it holds one. A USD-capable account lets the business take in the dollars directly and decide when to convert, instead of accepting whatever rate the bank applies on arrival.

For offshore-registered companies that bill Caribbean clients, holding the funds in a stable GBP or EUR balance through an FCA-authorised provider avoids forced conversion. EQWIRE's comparison of Wise Business and an FCA EMI for offshore companies covers how that setup works for non-UK entities sending money to the Eastern Caribbean or receiving from it.

Reconciliation is the step most finance teams overlook. Because the incoming amount can arrive short after correspondent deductions, the payment reference on the SWIFT message is what ties a part-paid invoice back to the original sum. Asking Caribbean clients to quote the invoice number in the reference, and recording the sender's bank and the value date, lets the team trace any shortfall in minutes rather than days.

The Real Cost of XCD Transfers

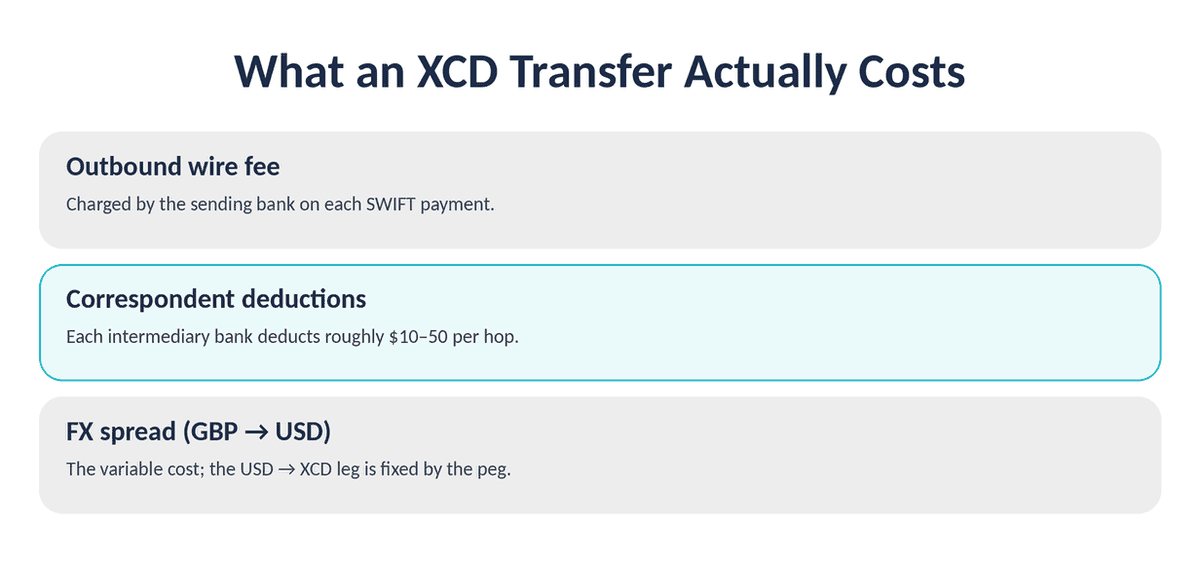

The headline transfer fee is rarely the real cost of East Caribbean dollar transfers. Three components stack up: the outbound wire fee, the deductions taken by correspondent banks along the way, and the FX spread applied when pounds become dollars.

[aa fast-fact]

Fast Fact: Each correspondent or intermediary bank in a SWIFT chain typically deducts between $10 and $50 per transfer, and a payment can pass through more than one before it arrives.

[/aa]

Intermediary and Correspondent Fees

Correspondent banks charge for passing a payment along, and those charges are deducted from the transfer in transit unless the sender chose the OUR code. Wise's breakdown of SWIFT correspondent fees explains how OUR, SHA, and BEN determine who absorbs them. With SHA or BEN, a £5,000 invoice can land short by $30–80, which forces awkward conversations with suppliers about the shortfall.

These deductions are the single most common hidden cost in payments to the region, and they are invisible on the sender's side until the recipient reports a smaller amount than expected. On one transfer the deduction looks minor. Across a month of supplier runs it compounds, and a business sending twenty payments can lose several hundred dollars to intermediaries alone, none of which shows on its own bank statement.

FX Spread and the Hidden GBP→USD→XCD Conversion

Because the route runs through dollars, a pound payment converts twice in concept: GBP to USD, then USD to XCD. The USD-to-XCD leg is fixed by the 2.70 peg, so the variable cost sits entirely in the GBP to USD spread the bank applies. A markup of even 1–2% on a large transfer outweighs the flat wire fee.

A UK company watching the GBP to XCD exchange rate should really watch the GBP to USD rate, since that is the only leg where the bank's margin lives.

[aa cta]

See Exactly What an International Transfer Costs

Hidden correspondent deductions and FX markups are easier to control when pricing is transparent from the start.

[aa btn]Create Account[/aa]

[/aa]

How Long XCD Transfers Take

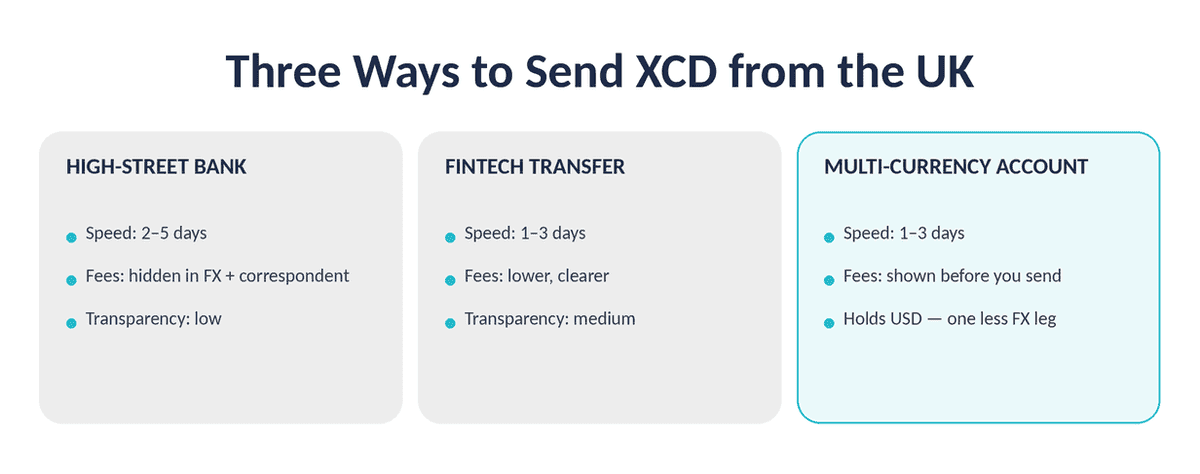

Correspondent SWIFT payments to the Eastern Caribbean usually settle in two to five business days, longer than a domestic transfer because of the extra hops and compliance checks. Industry data on how long SWIFT transfers take puts most cross-border payments in a one-to-five-day window, with correspondent-heavy corridors at the slower end.

Cut-off times add a hidden day. A payment instructed after the bank's afternoon cut-off, or close to a UK or US public holiday, only enters the SWIFT flow the next working day. Finance teams paying Caribbean suppliers on a deadline should send early in the week to leave room for a correspondent hold.

Tracking helps when a payment runs late. Most banks now support SWIFT gpi, which assigns each transfer a unique end-to-end reference and shows where the money is sitting in the correspondent chain. A finance team that quotes that reference can get a clear status from its bank instead of waiting blind, which shortens the time spent chasing a delayed East Caribbean dollar transfer.

How UK and Offshore Businesses Can Simplify XCD Payments

The cleanest fix for recurring XCD payments is to remove a step rather than chase a cheaper wire. Holding US dollars in a multi-currency account lets a business send dollars straight to the correspondent network and receive dollars without an arrival-day conversion, which eliminates one FX leg and makes the landed amount predictable.

An FCA-authorised electronic money institution can give a UK or offshore company a multi-currency account that sends and receives over SWIFT alongside local rails, with the correspondent route and charge codes shown up front. EQWIRE's look at SWIFT versus SEPA payout costs for businesses illustrates how rail choice and currency holding drive the total cost of cross-border payouts. For companies sending regular East Caribbean dollar payments, the combination of a USD balance and transparent fees turns an unpredictable wire into a routine transfer.

[aa cta]

One Account for All Your International Business Payments

Hold US dollars, send and receive over SWIFT, and see every fee before you confirm.

[aa btn]Open Business Account[/aa]

[/aa]

FAQ

How do UK and offshore businesses send or receive XCD East Caribbean dollars via SWIFT?

UK and offshore businesses send or receive XCD East Caribbean dollars via SWIFT by routing the payment through a US dollar correspondent bank rather than moving the currency directly. The sender's bank converts the funds to US dollars, transmits a SWIFT instruction to a correspondent bank in New York or Miami, and that bank forwards the dollars to the beneficiary's bank in the Eastern Caribbean, where they are credited in XCD at the 2.70 peg. To do this, the sender needs the beneficiary's SWIFT/BIC code, account details, the required intermediary bank, and a charge code (OUR, SHA, or BEN). Businesses that hold US dollars in a multi-currency account can shorten the chain by sending dollars directly, which reduces both FX cost and the risk of correspondent deductions.

Can you send XCD directly from a UK bank account?

No UK bank lets you send East Caribbean dollars directly. The payment is converted to US dollars and sent over SWIFT to a correspondent bank, then credited in XCD at the destination. The recipient's bank applies the fixed 2.70 peg when it converts the dollars to East Caribbean dollars, so the currency only becomes XCD at the very end of the journey.

Is the East Caribbean dollar freely convertible?

Yes. The East Caribbean dollar is freely convertible, and several member states, including Saint Lucia, operate without exchange controls. A UK business can pay into or receive from the region without capital restrictions. The practical limits are commercial rather than regulatory: routing through correspondent banks, fee deductions, and settlement time.

How much does it cost to send XCD from the UK?

A transfer carries three costs: the outbound wire fee from the sending bank, correspondent deductions of roughly $10–50 for each intermediary in the chain, and the FX spread on the GBP-to-USD conversion. On a typical business transfer, the FX spread and correspondent deductions usually outweigh the flat wire fee, so the cheapest headline fee is not always the cheapest transfer.

How long does an XCD transfer from the UK take?

Most correspondent SWIFT transfers from the UK to the Eastern Caribbean settle in two to five business days. Payments sent after a bank's daily cut-off, or near a UK or US public holiday, take longer because they only enter the SWIFT flow on the next working day. Sending early in the week leaves room for any correspondent compliance hold.

UK and offshore businesses can keep XCD East Caribbean dollar payments fast and predictable by understanding the route before they send. The currency's US dollar peg, its SWIFT-only path, and the correspondent banks in the middle all shape what a transfer costs and when it lands. Holding US dollars in a multi-currency account removes one FX leg and most of the surprise deductions, turning an opaque wire into a routine payment. For businesses that regularly send or receive across the region, mapping each currency's settlement window on the EQWIRE currency network is a practical first step toward lower-cost EC dollar payments.

Power your payments

with EQWIRE

Create your account in minutes and experience smooth, secure global payments.

" height="9.0156px" id="LIcbdboyB" transform="translate(4.987 4.5)" width="9.01562px"/></svg>)